Canadian employees are increasingly leaving small businesses, not just for higher salaries, but also for better access to extended health, dental, retirement, and mental health benefits that larger employers often provide. A December 2025 Robert Half Canada survey of more than 1,500 professionals found that “better benefits and perks” are the primary driver for employees seeking new opportunities, indicating a lasting change in what Canadian workers expect from their employers.

While small businesses form the backbone of the Canadian economy, they often struggle to compete on traditional benefits. However, they can bridge this gap by offering affordable and flexible benefits options, such as Health Spending Accounts and Group RRSPs, without requiring an enterprise-level budget.

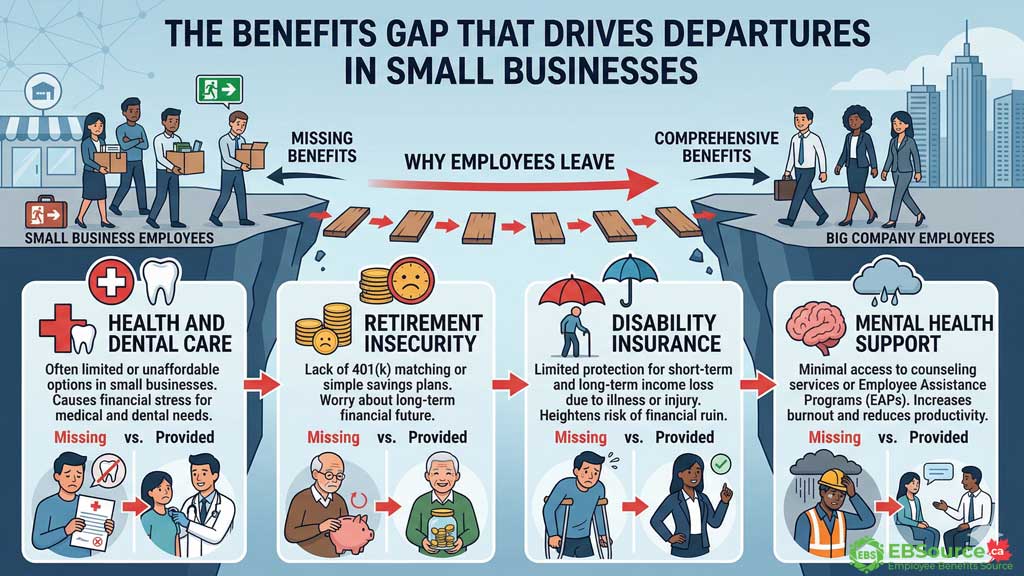

The Benefits Gap That Drives Employees to Leave Small Businesses

Extended health, dental, retirement savings, disability insurance and mental health support are top priorities for Canadian employees, and these are precisely the areas where small businesses often have the largest gaps.

These gaps create both immediate financial pressure and long-term uncertainty, making larger employers more attractive than others.

To understand why employees leave, it is important to break down where these gaps are most visible:

The Health and Dental Care Gap

Canada’s public healthcare system covers doctor visits and hospital stays, but leaves a massive gap in routine and essential care. Prescription drugs, dental work, vision care, and paramedical services (such as physiotherapy or massage therapy) are largely paid out of pocket unless an individual has private insurance.

An employee at a small business might pay much more for a necessary prescription compared to their friend working for a large corporation who has access to a group drug plan. This tangible, recurring expense is a constant reminder of what they are missing. It is no surprise that, in Blue Cross’s small business study, 76% of Canadian employees without health benefits would leave their jobs for one that offered them better benefits.

The Gap in Retirement Security

While day-to-day expenses create immediate pain, the lack of retirement support creates deep-seated anxiety about the future. Most large employers offer a Group Registered Retirement Savings Plan (RRSP) or a pension plan with an employer match, which compounds over decades.

Many small businesses, if they offer anything, provide only the administrative framework for a Group RRSP, with no employer contribution. An employee sees their peers at larger firms accumulating tens of thousands of extra dollars for retirement and knows they are falling behind. This gap in long-term financial security is a powerful incentive to find an employer who will co-invest in their future.

The Missing Safety Net: Disability Insurance

Beyond day-to-day health, employees worry about worst-case scenarios. What happens to their income if they get sick or injured and can’t work for months? What would their family do if they passed away unexpectedly?

Large companies have made short-term disability (STD), long-term disability (LTD), and basic life insurance standard components of their benefits packages. This safety net provides critical peace of mind, especially for employees with dependents or mortgages. For many small business employees, this protection is completely absent, leaving them feeling financially vulnerable and one emergency away from disaster.

The Insufficient Support for Mental Health

Mental health support has shifted from a “nice-to-have” perk to a core expectation, particularly for younger workers. Today, larger companies often offer an Employee Assistance Program (EAP), which provides confidential, free access to short-term counselling for issues ranging from stress and anxiety to financial and legal advice.

The Robert Half survey identified Gen Z workers (41%) and working parents (39%) as the groups most likely to be seeking new jobs. These are the same demographics that place the highest value on mental health resources. A business that offers no formal, confidential support for mental wellness sends a message that it considers mental health a low priority, pushing these in-demand workers toward employers who demonstrate a greater commitment to employee well-being.

The following table summarizes the typical coverage gap between small and large Canadian employers:

| Benefit Category | Small Businesses | Large Employers |

|---|---|---|

| Extended Health & Dental | Basic plan with higher co-pays, or no coverage at all. | Comprehensive plan with a broad drug formulary and low co-pays. |

| Retirement Savings | Group RRSP facilitation only, often without employer matching. | Defined Contribution Pension Plan or Group RRSP with an employer match. |

| Disability Insurance | Rarely included in small business plans. | Standard inclusion in most packages. |

| Mental Health Support | Usually absent or has very low annual limits. | Employee Assistance Program (EAP) included, plus dedicated mental health practitioner coverage. |

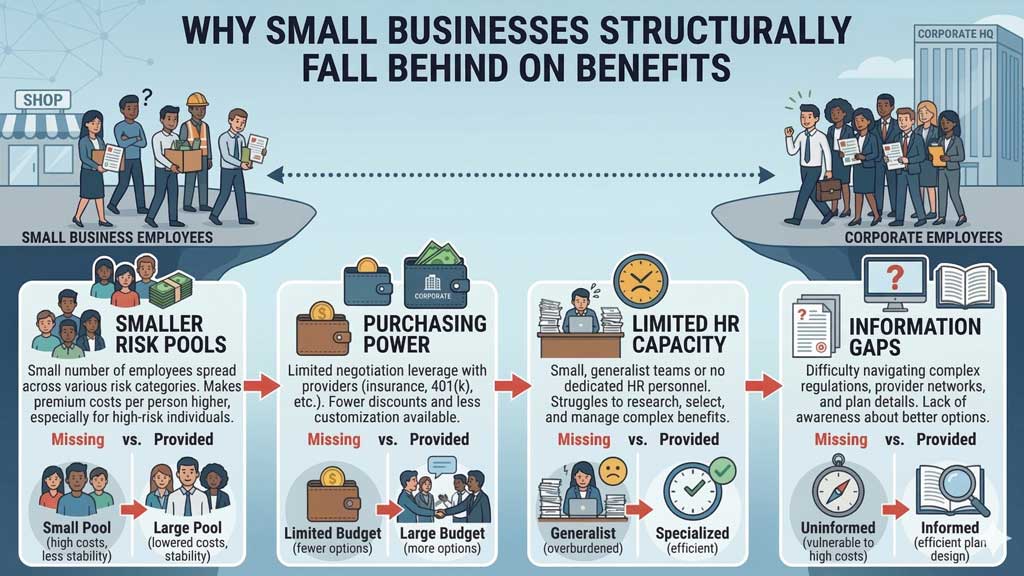

Why Do Small Businesses Struggle to Offer Competitive Benefits?

The struggle for small businesses to offer competitive benefits is not due to a lack of generosity but is rooted in structural disadvantages related to scale and access, including smaller risk pools, weaker purchasing power, limited HR capacity, and information gaps.

These structural challenges help explain why the benefits gap persists, and why employees ultimately decide to leave:

Smaller Risk Pool

In Canada, it can be difficult to find cost-effective health insurance plans for small groups of employees. From an insurance company’s perspective, a smaller employee group represent a higher risk. For example, a single high-cost claim in a firm with 10 employees can cause a significant spike in renewal premiums for the entire group, whereas the same claim in a 500-person firm would have a negligible impact.

Lower Purchasing Power

Larger groups spread risk across more members, making premiums more stable per employee, and businesses with more than 30 employees have higher negotiating power. The size of an employee pool influences premiums: larger groups often pay lower costs, so group health benefits for small businesses tend to cost more than for larger companies. As a result, many small firms may choose to reduce benefits to manage expenses effectively.

No Dedicated HR or Benefits Expertise

In many small firms, benefits administration falls to an owner or office manager who lacks the specialized expertise to evaluate insurance proposals, negotiate renewals, or effectively communicate the plan’s value to staff. Without that expertise, renewals go unchallenged, and employees never learn the dollar value of what they do receive.

Information Gaps

Many SME owners are unaware of flexible and cost-effective alternatives to traditional insurance. The assumption that “real” benefits require a large traditional insured plan leads many small employers to offer nothing at all. However, there are several options available, such as Health Spending Accounts, individual health and dental plans, and Wellness Spending Accounts, that can offer health benefits to both employers and employees.

These barriers are real, but none of them is unconquerable. Understanding them is the first step to working around them, and affordable solutions do exist, as covered in the next section.

What Affordable Benefit Solutions Can Help Close the Benefits Gap?

Small businesses can eliminate their most critical coverage gaps by leveraging Group Insurance Plans, Health Spending Accounts (HSAs), Wellness Spending Accounts (WSAs), Group RRSPs, and Employee Assistance Programs (EAPs). These flexible tools are often accessible to firms with as few as two employees, allowing even the smallest teams to provide high-value protection without a massive corporate budget.

Explore these 5 core options to find the right fit for your budget and your employees’ needs:

- Group Insurance Plan: The traditional option, offering pooled coverage for extended health, dental, vision, and disability. Plans are available in tiered packages (basic, standard, enhanced), allowing a business to start small and scale up.

- Health Spending Account (HSA): This is a tax-efficient plan. A properly structured HSA that qualifies as a private health services plan (PHSP) can let an employer reimburse eligible medical and dental expenses on a tax-advantaged basis. The employer only pays when a claim is made, providing complete cost control with no premiums. Employers looking for additional flexibility may also consider a Cost Plus Program to reimburse eligible healthcare expenses on a pay-as-you-go basis.

- Wellness Spending Account (WSA): A WSA provides a flexible, taxable allowance for employees to spend on a wide range of wellness and personal development categories, such as gym memberships, childcare, or professional courses.

- Group RRSP: This option lets employees contribute through payroll deductions, and some employers also add matching or direct employer contributions. Employer contributions are a deductible business expense.

- Employee Assistance Program (EAP): An EAP offers confidential, short-term counselling and support for mental health, financial, and legal issues. It is a very low-cost option that directly addresses the growing demand for mental health support.

Quick tip: If you are not ready for a full suite, a powerful starting combination for a small business is an HSA paired with an EAP. This covers both physical and mental health needs at a fraction of the cost of a full group insurance plan.

Beyond Benefits: Other Factors Pushing Employees Out

While the benefits gap is the primary driver, other structural realities like limited career advancement and workplace burnout also force top talent to look elsewhere.

Thus, small business owners must address these two additional challenges to keep their teams intact:

- Limited Career Advancement: As noted in the Robert Half survey, 23% of job seekers are motivated by a lack of advancement opportunities. Small businesses are naturally flatter, with fewer rungs on the corporate ladder. Ambitious employees often have to leave to get a promotion or a significant increase in responsibility.

- Burnout and Increased Demands: With smaller teams, employees are often required to wear many hats. This can provide valuable experience, but it can also lead to unsustainable workloads and burnout, another key factor cited as a driver of rising turnover.

In summary, employees are leaving small businesses because they feel financially and personally exposed. They are paying more for healthcare, falling behind on retirement savings, and lacking a safety net for their mental and physical well-being.

For small business owners, the solution is not to magically match a multinational corporation’s budget; first, acknowledge these specific pain points, then seek out smart, targeted, and affordable solutions that address them. Modern vehicles like Health Spending Accounts, Employee Assistance Programs, and Group RRSPs with a modest match are designed specifically for the realities of small businesses. By understanding exactly why their employees are leaving, owners can finally start offering compelling reasons for them to stay.