Many employers make avoidable mistakes when choosing employee benefits in Canada by focusing on short-term decisions instead of long-term plan performance.

Common mistakes include focusing on price rather than value, not assessing employee needs, failing to establish cost controls, investing too little in mental health coverage, ignoring compliance requirements, and not reviewing the benefits advisor or broker.

The following sections identify six mistakes and explain how to avoid them. This will help ensure that your employee benefits plan meets the needs of your workforce, stays cost-effective over time, and complies with Canadian regulations.

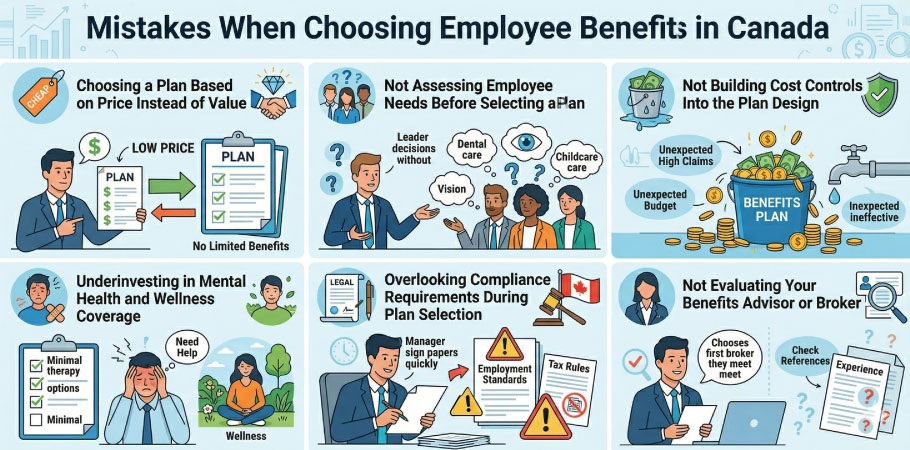

Mistake #1: Choosing a Plan Based on Price Instead of Value

Selecting a benefits plan based primarily on the lowest quoted premium is one of the most common and costly mistakes when choosing employee benefits. While a lower premium may appear attractive, it often reflects trade-offs in plan design.

These trade-offs typically appear as higher deductibles, tighter drug formularies, lower paramedical maximums, or narrower coverage categories. When these gaps emerge, employee satisfaction declines and the perceived value of the plan drops.

In some cases, employers may also make exceptions or cover expenses outside the plan, reducing or eliminating the savings created by the lower premium.

Instead of focusing only on price, it is more useful to look at the overall value of the plan. That means considering:

- Coverage depth across benefit categories

- Plan flexibility for different employee needs

- Insurer service quality and claims experience

- Cost changes over the long term at renewal

A plan that costs a bit more in the first year but provides good coverage and stable renewals can lead to better results over time. To avoid making a costly mistake, ask for a detailed comparison of benefits before choosing any plan.

Mistake #2: Not Assessing Employee Needs Before Selecting a Plan

Choosing a benefits plan without first understanding what employees actually need often leads to coverage gaps, low usage, and wasted spending.

Many employers rely on broker recommendations or internal budget assumptions without consulting the people who will use the plan. As a result, the selected coverage may not align with workforce priorities.

For example, a workforce with young families may receive strong individual coverage but limited dependent benefits. On the other hand, an older workforce may be placed in a plan that underdelivers on prescription drugs or vision care. In both cases, parts of the workforce do not receive adequate support, no matter how much money is spent.

The root issue is that benefit needs vary significantly across different groups. Age, family situation, and even location all influence which types of coverage employees value most. When employers ignore these factors, they often choose standard plan designs that do not meet the needs of their actual workforce.

Mistake #3: Not Building Cost Controls Into the Plan Design

Plans without built-in cost controls remain one of the most frequent mistakes when choosing employee benefits. Even when coverage matches employee needs, unmanaged claims growth can lead to steep premium increases at renewal.

Group benefits premiums change each year based on claims experience, drug costs, and utilization patterns. When a plan has no built-in cost controls, higher claims directly translate into higher renewal rates. Plans with open-ended limits, no co-payments, and no usage incentives often experience premium increases that outpace business growth within a few years.

The best time to control costs is during plan selection. Four cost-control features can be built into the design from the start, including:

- Co-payments that share costs between the employer and the employee

- Generic drug substitution policies

- Combining a lean core plan with a Health Spending Account (HSA)

- Regular reviews to adjust coverage limits

These strategies help control the growth of claims while still providing good coverage. Employers that implement cost controls early usually have more stable premiums and face fewer drastic increases in renewal costs.

Mistake #4: Underinvesting in Mental Health and Wellness Coverage

Mental health coverage is often overlooked, making it one of the most common mistakes when choosing employee benefits.

Mental health conditions are one of the leading causes of disability claims and workplace absence in Canada. The Centre for Addiction and Mental Health notes that mental illness affects people across all ages, education levels, income levels, and cultures, and that the economic burden of mental illness in Canada is substantial.

Despite this, many employers choose plans with limited counselling coverage or no mental health support at all. When coverage is insufficient, employees may delay treatment or pay out of pocket, increasing absenteeism, disability claims, and turnover.

Mental health coverage should be evaluated during plan selection. Three key components to compare include:

- Employee and Family Assistance Programs (EFAPs) offering confidential short-term counselling

- Paramedical counselling coverage for psychologists, social workers, or psychotherapists

- Wellness Spending Accounts (WSAs) for mental health and stress-related expenses

Plans that offer access to Employee and Family Assistance Programs (EFAP) with strong counselling options provide better support for employees and help manage long-term costs.

To avoid making a mistake, consider mental health coverage as a key factor when comparing plans. Choosing a plan with solid mental health support can lower absenteeism, boost productivity, and enhance workforce wellbeing.

Mistake #5: Overlooking Compliance Requirements During Plan Selection

Overlooking compliance requirements is one of the most costly mistakes when choosing employee benefits, particularly for employers focused only on coverage and pricing.

Employee benefits in Canada are governed by employment standards, insurance contract rules, and tax regulations. Employers who focus only on coverage and pricing may overlook these requirements and unintentionally create compliance risks.

To avoid this mistake, review compliance requirements before selecting a plan. Key items to confirm include:

- Benefit continuation during statutory leaves

- Tax reporting obligations for employer-paid benefits

- Applicable employment standards affecting eligibility or coverage

Reviewing these requirements during plan selection helps avoid administrative issues and ensures the plan can be implemented correctly from day one. If you are a new entrepreneur in this industry, it is advisable to discover how to budget employee benefits for the first time.

Mistake #6: Not Evaluating Your Benefits Advisor or Broker

If you accept a broker’s recommendation without checking how they get paid, their process, and their level of service, you might end up with coverage that does not fit your needs and costs that keep rising.

Many employers treat their relationship with advisors as a one-time event. After they set up the plan, support often stops until it is time for renewal. This leaves employers without help in managing costs, staying compliant, or improving their plans.

It is also important to understand how your advisor is paid. Most advisors earn commissions based on premiums, which could lead to conflicts of interest. Knowing how your advisor gets paid can help ensure that their suggestions meet your business needs.

Before selecting a plan, evaluate your advisor by confirming:

- How the advisor is compensated

- Which insurers they compare and whether any are excluded

- What reporting and renewal analysis do they provide

- Whether compliance and enrolment support is included

- Who will handle the day-to-day service after implementation

Choosing an advisor who provides transparent compensation and ongoing support helps ensure better plan performance over time.

How Do You Manage Your Benefits Plan After Selection?

Avoiding mistakes when choosing employee benefits does not end after selecting a plan. Ongoing administration, employee education, regular reviews, and funding decisions all influence whether the plan delivers lasting value.

Key areas to focus on after your plan is in place include:

Avoiding Plan Administration Errors After Setup

The most common administration errors (late enrolments, missed terminations, and eligibility mismatches) are also the most preventable. To avoid unnecessary expenses and ensure our policies cover only eligible employees, it is important to enroll and terminate employees on time.

To reduce these risks:

- Include benefits steps in onboarding and offboarding checklists

- Set HRIS reminders for eligibility dates

- Review monthly insurer invoices against employee records

Educating Employees to Maximize Plan Value

A well-designed plan that employees do not understand delivers a fraction of its potential value and generates frustration that undermines the employer’s investment.

At a minimum, employees should understand:

- What services are covered

- How to submit claims

- annual and per-service limits

- when pre-authorization is required

These topics should be addressed during onboarding for new hires and revisited at least once a year for the full team, ideally before the renewal period when any changes to coverage take effect.

Reviewing and Updating Your Plan Regularly

Workforce needs and claims patterns change over time. Plans that are not reviewed regularly may become misaligned with both employee needs and budget constraints.

A practical review cadence includes a full review before each renewal and a mid-year check-in. These reviews should assess usage trends, cost changes, employee feedback, and potential plan adjustments.

Your benefits advisor should support this process. If reviews are not proactively scheduled, it may be a sign to reassess the level of ongoing advisory support.

Tax Treatment of Employer-Paid vs. Employee-Paid Premiums

Who pays benefits premiums can affect whether coverage is taxable and how claims are treated. Tax treatment varies depending on plan design, funding structure, and jurisdiction.

Employer-paid extended health and dental coverage is generally not considered a taxable benefit at the federal level when provided through a qualifying private health services plan. However, provincial rules may differ. In Québec, employer contributions to group insurance plans, including health and dental coverage, are typically treated as a taxable benefit for provincial income tax purposes.

For disability coverage, tax treatment depends on how the plan is funded. When employees pay the premiums, benefits received during a claim are generally tax-free. If the employer pays the premiums, benefits are typically taxable. Mixed funding arrangements may result in partially taxable benefits.

Confirm the tax treatment of each benefit category before finalizing plan funding arrangements to avoid unexpected payroll reporting or employee tax implications.

FAQs about Mistakes When Choosing Employee Benefits in Canada

Why is it a mistake to copy another company’s employee benefits plan?

Every workforce has different demographics, needs, and priorities. Copying another company’s plan may leave your employees with coverage they don’t value while overpaying for benefits that don’t apply to your team’s situation.

Is it a mistake to choose the cheapest employee benefits plan available in Canada?

Yes. The lowest-cost plan often comes with high deductibles, limited coverage, and exclusions that frustrate employees. Poor benefits can hurt recruitment and retention, which ends up costing far more than a slightly higher premium.

What is the mistake of ignoring flexible benefits options for a diverse Canadian workforce?

A rigid, inflexible plan fails to account for the varying needs of a multi-generational or multicultural workforce. Flexible or modular benefits allow employees to customize coverage, increasing satisfaction and perceived value without dramatically increasing costs.