Severance pay is a critical financial safeguard for Canadian employees who are terminated without cause or laid off; it protects employee rights and provides essential assistance during unexpected job transitions.

Whether you qualify for this payment depends on your jurisdiction, your length of service, and, especially in Ontario, your employer’s payroll size. Federal employees face a different threshold under the Canada Labour Code.

While statutory formulas set the minimums, common law often yields significantly higher entitlements based on age, role, and other factors. Severance pay is taxable income, and how it is taxed depends on whether it is paid as a lump sum, as a salary continuance, or transferred to an RRSP.

Understanding how severance is calculated, the tax implications, and the exemptions is key to maximizing your settlement and easing the transition to your next role.

What is Severance Pay?

Severance pay is compensation provided to eligible employees for the loss of a job through no fault of their own. Termination without cause is typically the most frequent trigger for this obligation; it includes being let go due to corporate downsizing, organizational restructuring, or a business closure.

In addition to direct layoffs, other scenarios may mandate a severance payout, including constructive dismissal, temporary layoffs (Ontario), and resigning after receiving a termination notice.

- Constructive dismissal: This occurs when your employer makes significant changes to your employment conditions that effectively force you to resign. Some examples include demotions, pay cuts, and relocated workplaces.

- Temporary Layoffs (Ontario-only): Under Ontario’s law, a temporary layoff is legally deemed a termination if you are laid off from your job for 35 weeks or more in 52 weeks, even if the time is not consecutive.

- Resigning After a Termination Notice: This is when you have already been given a formal termination notice, but choose to resign before your final day and still retain your severance rights, provided you give the employer at least two weeks’ notice. (Note: In Quebec, if you resign before the employer’s termination date, you may lose the indemnity for the remaining notice period.)

Severance pay is a distinct legal concept from termination pay, which compensates an employee for the minimum notice period the employer is required to give them before their job ends.

When you meet specific criteria under employment standards legislation, severance pay becomes mandatory. However, not every terminated employee qualifies. The specific eligibility rules, calculation formulas, and caps differ depending on which jurisdiction applies to your work.

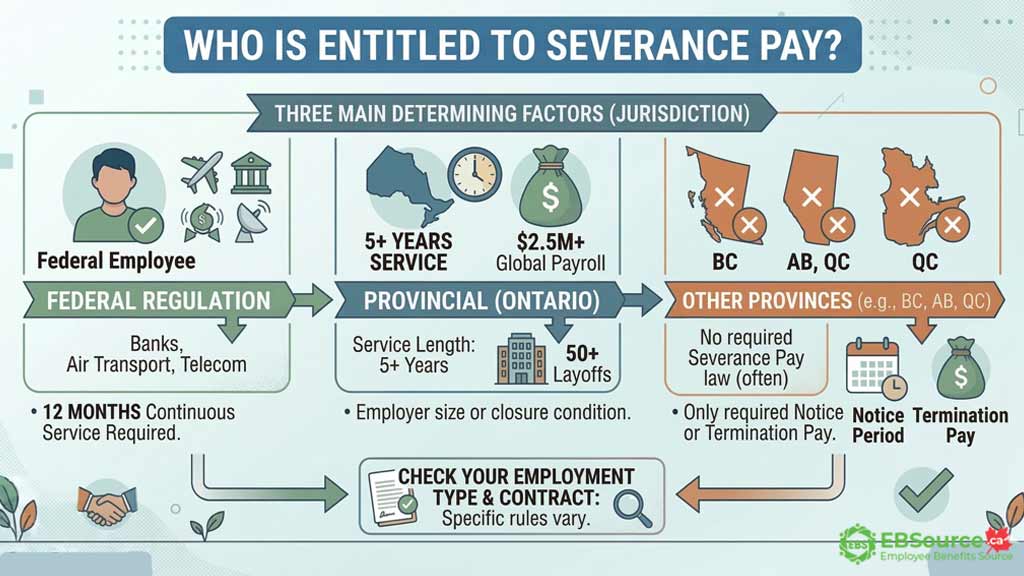

Who is Entitled to Severance Pay in Canada?

Eligibility for severance pay depends on whether you fall under federal or provincial jurisdiction, how long you have worked, and whether your employer meets specific payroll or headcount thresholds.

Employees in federally regulated sectors such as banking, air transportation, and telecommunications must have 12 months of continuous service to be entitled to severance pay under the Canada Labour Code.

Meanwhile, in Ontario, under the Employment Standards Act, an employee qualifies for severance pay if their employment is severed and they have worked for the employer for 5 or more years (whether continuously or not). In addition, one of the following two employer conditions must be met:

- The employer has a global payroll of at least $2.5 million.

- The employer has severed the employment of 50 or more employees within six months because all or part of the business has permanently closed.

In some other provinces, such as British Columbia, Alberta, and Quebec, there is no separate statutory severance pay like Ontario; only termination pay or notice is required.

How Much Severance Pay You Get: Statutory vs. Common Law

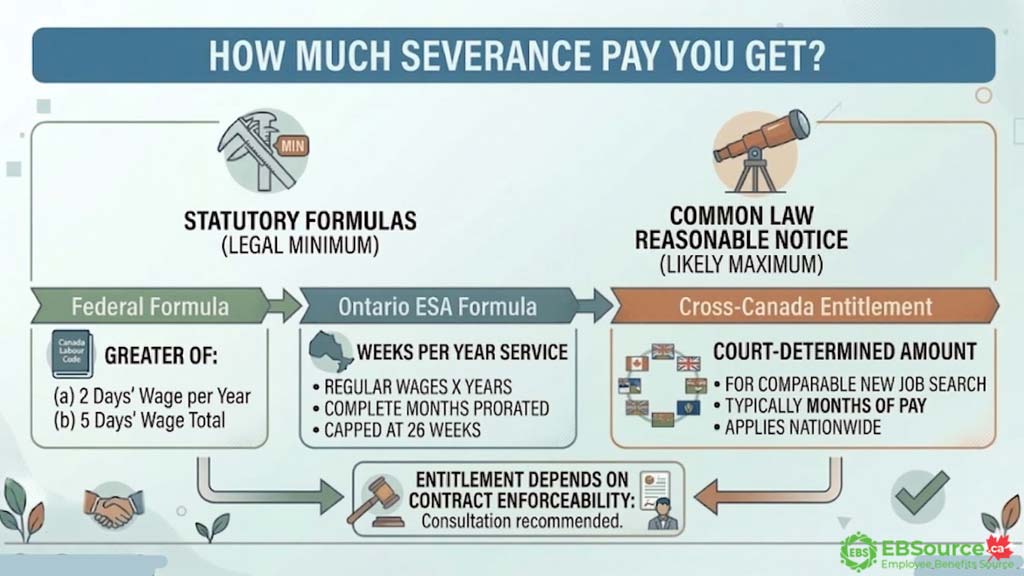

The amount of severance you receive is generally determined by two different legal frameworks: statutory formulas (the legal minimum) and common law reasonable notice (the likely maximum).

While the gap between these two figures can be significant, the calculation always begins with the mandatory minimums set by provincial law:

Statutory Formulas: The Floor

Statutory severance formulas differ sharply between federal and Ontario rules, and the federal formula produces a much smaller payment than Ontario’s ESA formula for employees with equal service. The two calculations are:

- Federal Formula (under section 235(1) of the Canada Labour Code): the greater of (a) two days’ wages at the employee’s regular rate for regular hours of work for each completed year of employment, or (b) five days’ wages at the employee’s regular rate.

- Ontario’s ESA Formula: regular weekly wages multiplied by years of service, capped at 26 weeks. Incomplete years are prorated: you divide the number of complete months in the final partial year by 12 and add that fraction to your completed years.

The following table compares the two statutory formulas side by side:

| Element | Ontario (ESA) | Federal (Canada Labour Code) |

| Formula | 1 week of regular pay per year of service (prorated for partial years) | Greater of 2 days per completed year or 5 days total |

| Maximum | 26 weeks | No statutory cap on the number of days |

For qualifying Ontario employees, the statutory severance entitlement is substantially larger than the federal formula in most mid-career scenarios. An employee with 10 years of service, for example, receives 10 weeks under the Ontario ESA but only 20 days under the federal formula. However, both formulas represent only the statutory minimum, and common law reasonable notice, covered in the next section, frequently exceeds either figure by a wide margin.

Common Law Reasonable Notice: Beyond the Statutory Minimum

Unless you have a valid and enforceable termination clause in your employment contract, you are entitled to “common law reasonable notice”. It is a separate, court-determined entitlement that typically yields months of compensation rather than the weeks provided by statute. It is designed to provide you with enough financial security to find a comparable new job.

In many cases, court-awarded notice is measured in months, but the range depends on your province, role, tenure, and job market. In practice, common law awards can range from 3 months for short-service junior employees to 24 months for long-serving senior employees.

Other Factors That Influence Severance Pay Amounts

While the calculations above determine the basic statutory severance, the final severance amount is often influenced by the role’s specialization, the loss of non-salary benefits, and the validity of termination clauses in the employment contract.

These factors can shift an employee’s entitlement from the bare legal minimum to a much higher standard:

- Type of work: The law recognizes that some roles are harder to replace than others. Employees in highly specialized positions or with significant management responsibilities often justify higher compensation.

- Benefits: The discontinuation of benefits upon termination may warrant additional compensation.

- Invalid termination clauses: If the termination clause in your employment contract is invalid or unenforceable, you may be entitled to more than what is stated.

If an employer does not pay employees what they are owed or fails to meet the legal minimum, employees can file a complaint or take legal action.

How Severance Pay Is Taxed in Canada?

Severance pay counts as employment income for tax purposes, subject to your marginal tax rate. The Canada Revenue Agency treats it the same as wages earned from work.

Your employer will deduct income tax from your severance pay, and the rate depends on how much you receive and the payment method. The three primary ways severance pay is provided to employees are lump-sum payment, salary continuance, and direct RRSP transfers.

Here is how each type of method works and its tax treatment:

- Lump-sum payment: If you receive your severance as a single, one-time payment, the CRA considers it a retiring allowance, and your employer will be required to withhold tax at a flat rate.

- Salary continuance: If your severance is paid out as regular pay cheques over time, it is taxed as normal employment income. This means CPP, EI and income taxes are deducted as regular payroll.

- Direct RRSP transfers: You can request that employers transfer the severance amount directly into a Registered Retirement Savings Plan (RRSP) account, often without immediate withholding if it is within the eligible portion or within your available RRSP room for non-eligible amounts.

Note: If your employer agrees, splitting payments across tax years by receiving severance in two parts, one this year and one next, may help keep you in a lower tax bracket. However, failure to make payments as scheduled will immediately make the full remaining amount due.

How to Maximize Your Severance Pay

To get the most out of your severance pay, you should move beyond legal minimums by resisting artificial deadlines, calculating the true common law value, prioritizing legal counsel over basic regulatory advice, and challenging “for cause” designations or invalid contracts.

Follow these six tips to ensure you receive every dollar you are owed:

- Ignore employer deadlines: There are no legal time limits to accepting a severance offer. Don’t let false deadlines pressure you.

- Calculate using an online severance calculator: Get a rough estimate of what you are legally owed before accepting any offer.

- Consult an employment lawyer: Have an expert review before signing anything.

- Don’t contact the Ministry of Labour first: The Ministry can only provide minimums. They can help you pursue your full common law entitlements.

- Question termination for cause: Many supposed performance issues are pretenses to avoid paying severance.

- Review your employment contract: Many contracts have invalid termination clauses that cannot supersede common law.

Severance pay laws in Canada are complex, but vital to understand if you find yourself unfairly terminated or laid off. Taking the time to calculate what you are owed based on your specific situation and working with an employment lawyer to review any severance offers or employment contracts is crucial to receiving fair compensation.

FAQs on Severance Pay in Canada

What is considered regular wages for severance pay?

For salaried employees, regular wages are based on typical weekly earnings. For commission or variable pay, it is calculated using the average earnings over the last 12 normal weeks worked.

Where is severance pay regulated in Canada?

Severance pay is regulated through a combination of provincial and federal legislation, as well as common law precedents set by prior court decisions.

Why does severance pay increase under common law?

Common law takes into account many factors like age, salary, benefits lost, and ease of finding new work that increase severance amounts beyond basic statutory minimums.

Can employers avoid paying severance with termination clauses?

Sometimes, but many contract termination clauses are unenforceable if they contradict common law entitlements.

Is severance pay considered taxable income?

Yes, severance pay is considered employment income and is subject to tax withholdings and deductions.