Canada Pension Plan (CPP): Contributors, Monthly Payments, Contribution Rates

The Canada Pension Plan is a mandatory benefit for most Canadian employees, except those in Quebec. Workers aged 18 to 64 who earn over $3,500 a year usually have to contribute to CPP, with employers matching these contributions. However, if a worker is between 65 and 69 and already getting a CPP/QPP retirement pension, they can choose to stop paying by submitting Form CPT30 or keep paying. CPP contributions end at age 70.

In return for these contributions, the maximum monthly CPP retirement pension at age 65 is $1,507.65, while the average for new beneficiaries is $925.35. These amounts will increase gradually as CPP enhancements raise income replacement from 25% to 33% of pensionable earnings.

To fund both current and future pensions, the employee and employer contribution rate for 2026 is set at 5.95% on pensionable earnings between $3,500 and $74,600. Additionally, there is a CPP2 rate of 4% on earnings between $74,600 and $85,000. Earnings below $3,500 are exempt from contributions.

For more details on CPP, the article below covers contributors, contributions, benefit amounts, the payment schedule, and how to contact Service Canada.

What is the Canada Pension Plan?

The CPP is a retirement plan in Canada that provides income when people retire, become disabled, or pass away. It is the second part of Canada’s three-part retirement system, working alongside two other sources of income, which also include OAS/GIS, as well as private savings and workplace pensions. Most workers and self-employed individuals in Canada can participate, except for those in Quebec.

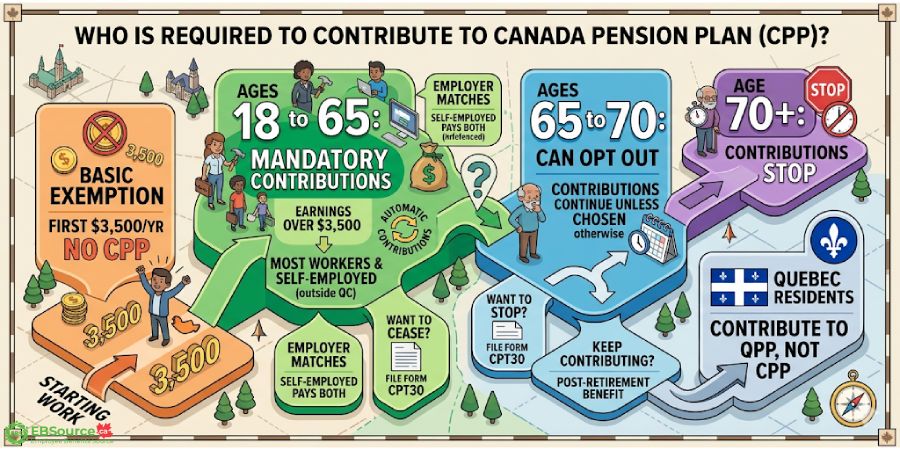

Who is Required to Contribute to the Canada Pension Plan?

Contributions to the CPP are mandatory for most workers aged 18 to 64 who earn more than $3,500 annually in Canada, excluding Quebec, with both employees and employers sharing the cost equally. On the other hand, self-employed individuals are responsible for paying both portions of the contribution. While the rules are generally straightforward, some details may vary based on employment type and age group.

Here are the key rules regarding eligibility for CPP contributions:

- Workers aged 18 to 65 must contribute on earnings over $3,500 per year.

- Workers aged 65 to 70 can opt out of contributions.

- Workers in Quebec contribute to the Quebec Pension Plan instead of the CPP.

For workers between the ages of 65 and 69, contributions will continue automatically unless the individual actively chooses to stop. To cease contributions, an employee in this age group must file Form CPT30 with their employer.

If they decide to keep contributing, the additional contributions will result in a post-retirement benefit in addition to their existing retirement pension. After reaching age 70, contributions stop entirely, regardless of whether the individual is still working.

The funds collected are used to pay current benefits and are also invested to meet future obligations, ensuring the sustainability of the plan over the long term.

How much is a CPP Payment per Month?

The CPP offers monthly benefits for retirement, disability, survivors, and children, along with a death benefit. The amount you get depends on how much you paid in, how much you earned, and when you start getting the payments.

As of January 2026, the average monthly retirement pension for new recipients is $925.35. For those under 65 with serious disabilities, the average monthly disability benefit is $1,210.86. Besides, a surviving spouse or common-law partners under 65 can receive an average survivor’s pension of $334.24. Those who are aged 65 or older also receive $334.24. And, the CPP child benefit is $307.81 per month for each child under 18 and for full-time students aged 18 to 25, whereas part-time students aged 18 to 25 receive a reduced benefit of $153.91 per month.

There is also a CPP death benefit, which provides a basic amount of $2,500, with an additional $2,500 available in some cases for deaths after January 1, 2025. The total maximum benefit is $5,000. The payment is usually made through the deceased’s estate, but if there is no estate or the executor has not applied, eligible individuals can apply in a specific order.

The table below summarizes the average and maximum amounts for commonly claimed CPP benefits in 2026:

| Benefit type | Average for new beneficiaries (Jan 2026) | Maximum monthly (2026) |

| CPP Retirement Pension (at age 65) | $925.35 | $1,507.65 |

| CPP Disability Benefit | $1,210.86 | $1,741.20 |

| CPP Survivor’s Pension (65 and older) | $334.24 | $904.59 |

| CPP Children’s Benefit | $153.91 for part-time students aged 18-25 | $307.81 |

| CPP Death Benefit (one-time payment) | $2,500 | $5,000 |

CPP benefits and payment amounts

Beyond that, the CPP offers 2 additional benefits: about $11.93 per month for post-retirement benefits and around $610.46 per month for post-retirement disability benefits.

The specific details regarding these benefits are as follows:

- CPP Post-Retirement Benefit: Earns about $11.93 monthly while working after retirement, up to $54.69 maximum.

- CPP Post-Retirement Disability Benefit: Offers $610.46 monthly if you become severely disabled.

Beyond that, if eligible for both a survivor’s and a retirement pension, the average combined benefit is $1,140.69, with a maximum of $1,531.56 per month.

The maximum CPP benefit amounts are expected to increase each month due to the enhancements that began in 2019. The figures provided reflect the maximum benefits starting in January 2026, and pensions beginning in later months of 2026 will have slightly higher maximum amounts. So you can use My Service Canada Account to view your personal estimate.

Note: CPP benefits are paid out monthly on the third-to-last business day of each month. More information is available in our article about CPP payment dates.

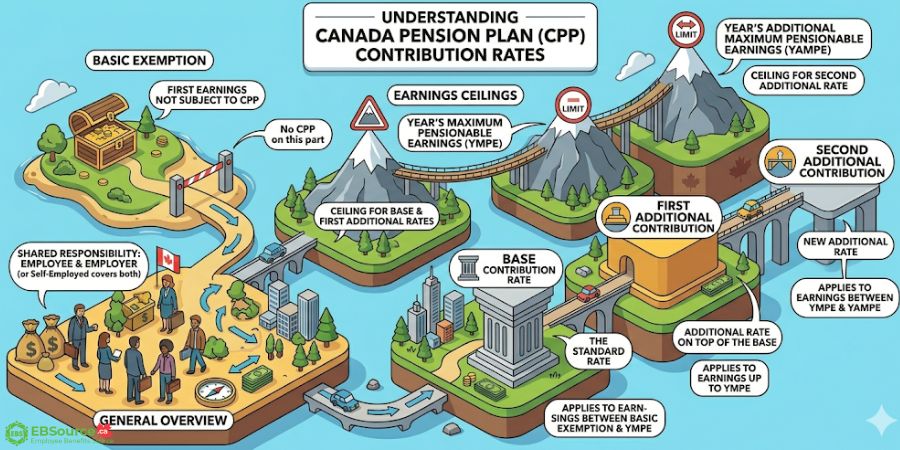

What are the CPP Contribution Rates?

Technically, CPP contributions are calculated using 3 rate tiers: the base contribution rate, the first additional contribution, and the second additional contribution, all of which apply to pensionable earnings. For the 2026 calendar year, both workers and employers will contribute 5.95% to the CPP on earnings over $3,500, up to a maximum of $74,600. Also, an additional CPP2 payment of 4.00% will be applied to earnings between $74,600 and $85,000.

Technically, CPP contributions are calculated using three rate tiers that apply to pensionable earnings. These earnings have two annual limits that change with wage growth in Canada. Each tier helps fund different future benefits, while the limits decide how much of a worker’s income can be contributed.

Below are the 3 CPP contribution rates:

Base Contribution Rate: The standard CPP rate is 4.95% for both employees and employers, applied to earnings between a basic exemption and the YMPE. These funds account for about 25% of your pensionable earnings.

First Additional Contribution: From 2019 to 2023, the rate increased by 1%, raising the total employee rate to 5.95% for earnings up to the YMPE. Employers also contribute at this rate. Self-employed individuals pay a total of 11.9% since they cover both employee and employer rates. This additional contribution helps enhance retirement income.

Second Additional Contribution: This new tier introduces a 4% contribution rate on pensionable earnings for both employees and employers, specifically for earnings between the YMPE and the YAMPE. For self-employed individuals, the rate is 8% for this same earnings range. There is no basic exemption for this tier.

Basic exemption and earnings limits for CPP contributions

These earnings have a basic exemption and two annual limits that change with wage growth in Canada. Each tier helps fund different future benefits, while the limits decide how much of a worker’s income can be contributed.

The detailed earnings ceilings are as follows:

Basic Exemption: The first $3,500 of annual earnings is exempt from CPP contributions. Therefore, the maximum annual employee contribution for 2026 is $4,230.45, while self-employed individuals can contribute up to $8,460.90.

Year’s Maximum Pensionable Earnings: The YMPE sets the maximum earnings for CPP contributions. In 2026, it is $74,600, up from $71,300 in 2025.

Year’s Additional Maximum Pensionable Earnings: The YAMPE serves as the second earnings ceiling. For 2026, the YAMPE is set at $85,000. Earnings exceeding the YAMPE are not subject to CPP contributions. As a result, the maximum annual employee second additional contribution for 2026 is $416 (calculated as $10,400 multiplied by 4%), while self-employed individuals will have a maximum contribution of $832.

How Can You Maximize Your Canada Pension Plan Benefits

While the CPP forms the foundation of your retirement income, your choices regarding when to apply, sharing options, and whether to continue working can optimize the benefits.

Here are three innovative strategies:

Choosing the Right Time to Apply

The age at which you apply for CPP determines your benefit amount for life, so timing is critical. While 60, 65, and 70 are typical ages, you can apply anywhere between 60 and 70. You should consider:

- If you apply before 65, benefits are reduced by 0.6% per month early. At 60, this equals 36% lower benefits.

- If you delay applying beyond 65, benefits increase by 0.7% per month late, up to a maximum increase of 42% at age 70.

Your decision depends on your current cash flow, health outlook, planned retirement activities, and life expectancy.

If you apply for a retirement pension after turning 65, Service Canada can issue retroactive payments for up to 12 months (11 months plus the month of application), but payments will not begin earlier than the month following your 65th birthday. No retroactive payments are available if you start receiving your retirement pension before age 65.

Note: You can apply for CPP online, by mail, or in person. The process is the same for all methods, and you will need to provide the same information no matter how you apply.

Sharing Your Pension with Your Spouse

If you and your spouse or common-law partner are CPP contributors, you may benefit from sharing your CPP pensions. CPP pension sharing does not increase the total benefits a couple receives. It just alters how the pension is divided between spouses or common-law partners, and it may help reduce taxes in some cases. Keep in mind that the CPP post-retirement benefit cannot be shared.

Continuing to Work While Receiving Your Pension

Thanks to the post-retirement benefit, you can continue contributing to the CPP while receiving your retirement pension. Working and making CPP contributions past age 65 increases future benefit payments.

It is optional to stop working to receive your CPP pension. Continuing to earn CPP credits allows you to augment your CPP income down the road.

Also, staying active and working in retirement have mental and physical health benefits.

How to Contact Service Canada about the CPP

Service Canada provides contact options for CPP inquiries by phone, online, mail, or in person. Average phone wait times were around 39 minutes in early 2026. Choosing the right channel for your question can save significant time, especially during peak periods.

Details on the CPP contact information are:

Phone: The main phone number for CPP is 1-800-277-9914 for callers in Canada and the U.S. If you are outside these countries, call 1-613-957-1954 collect. TTY users can reach Service Canada at 1-800-255-4786.

My Service Canada Account: For routine inquiries, use MSCA as it is the easiest option. You can check your CPP Statement of Contributions, payment details, update your address or direct deposit info, and download tax slips anytime without having to call.

eServiceCanada: If you need to talk to an agent but do not want to wait on hold, you can request a callback through eServiceCanada online. They will call you back within 2 business days. This is helpful for questions about your application status, benefit amounts, or contribution history that are not urgent.

In person: You can go to any Service Canada Centre in Canada for in-person assistance. This is helpful if you need help with forms, have complicated questions about your eligibility, or prefer face-to-face service. Check Canada.ca for the nearest location and hours.

By mail: You can find mailing addresses for each province on the Contact CPP page at Canada.ca. Use mail to send completed forms or documents if you can not submit online. Allow a few weeks for processing when using mail.

History and Purpose of the Canada Pension Plan

The Canada Pension Plan is a cornerstone of Canada’s retirement income system. It was established in 1966 through the Canada Pension Plan Act to provide a base retirement pension to employed Canadians in every part of the country.

Before the CPP, Canada had no nationwide government-sponsored retirement pension plan. Only 40% of the labour force had workplace pensions, leaving many seniors financially vulnerable. The CPP was introduced to change that by providing a reliable and portable source of retirement income to employed Canadians, regardless of their employment history.

The CPP aims to replace about 25%-33% of the average industrial wage for Canadians who contributed adequately during their working years. Along with Old Age Security (OAS) and private savings, the CPP ensures a basic income in retirement.

FAQs on the Canada Pension Plan

What is the difference between CPP and QPP?

The Quebec Pension Plan (QPP) is similar to the CPP but applies only to residents of Quebec. Workers in Quebec contribute to the QPP instead of the CPP. The plans have minor differences in contribution rates and administration.

Why should I check my CPP Statement of Contributions?

Reviewing your statement periodically ensures your contributions and pensionable earnings are reported accurately. This affects your future benefits, so any errors should be reported to CPP right away.

Do CPP benefits get taxed?

Yes, CPP retirement, disability, and survivor benefits are considered taxable income. Beneficiaries must report CPP income on their tax returns.

Can I receive CPP if I move outside Canada?

Yes, CPP retirement and disability pensions can be paid to eligible recipients who live outside Canada. Some benefits have residency requirements.

Can I collect CPP if I never worked?

No, CPP requires at least one contribution. However, you may qualify for survivor benefits if your spouse contributed. Non-working spouses should consider voluntary RRSP contributions or spousal RRSPs for retirement income.

Can I receive CPP while living outside Canada?

Yes, CPP payments continue worldwide without residency requirements. Notify Service Canada of address changes. Some countries have tax treaties affecting withholding rates. Direct deposit works internationally with proper banking information.

Where can I find my CPP Statement of Contributions?

Access your statement through My Service Canada Account online. Paper statements stopped in 2013 but remain available upon request. Review annually for accuracy, comparing against T4 slips. Report discrepancies immediately to protect future benefits.

Does divorce affect my CPP benefits?

If you earned CPP credits while married or in a common-law relationship, you can usually split them equally if you separate. The rules depend on your relationship type and when it ended.

For example, if your divorce or annulment happened on or after January 1, 1987, there is usually no time limit for splitting credits. But if a common-law relationship ended on or after that date, you generally have 48 months to apply, unless this limit is waived.

Since the rules can vary depending on your situation, check the official CPP credit-splitting page for the most accurate details, rather than relying on a single deadline.

What happens if I overpay CPP contributions during the year?

Overpayments happen when you work for multiple employers in a year, and each deducts CPP contributions without knowing what the others have deducted. When you file your annual tax return, the CRA checks if your total contributions were over the yearly limit and issues a refund if they were. The CPP Act allows for these refunds.

Disclaimer: CPP rules and payment amounts change depending on the type of benefit, the worker’s age, whether they are already receiving CPP or QPP retirement benefits, and the official rate period shown on Canada.ca. This page is only a planning guide and does not offer legal, tax, or financial advice. Please check the latest rules on the CRA or Service Canada website before making any decisions.