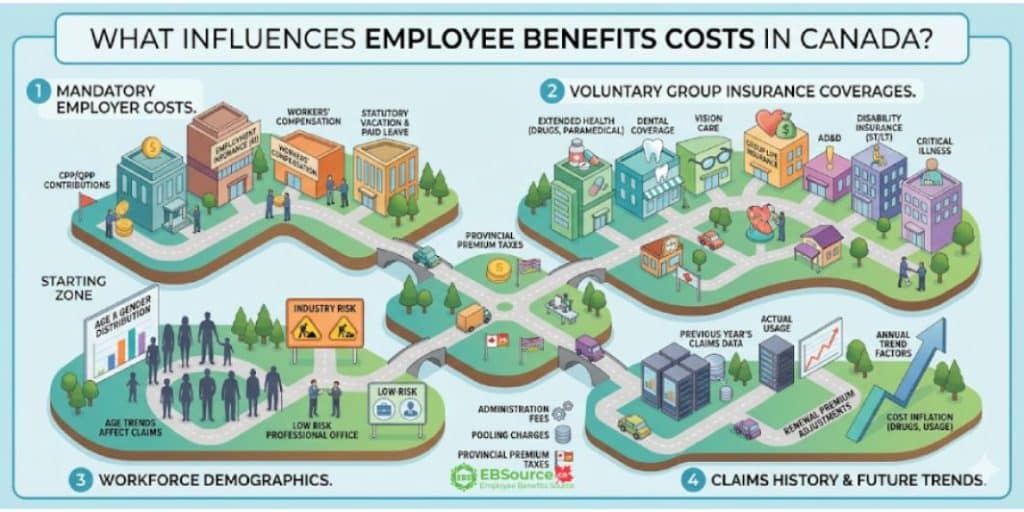

When creating a budget for employee benefits for the first time in Canada, there are two main cost layers to consider. The first layer includes mandatory payroll obligations, such as CPP contributions, EI, workers’ compensation, and statutory leave. The second layer consists of optional group insurance coverages, which include extended health, dental, vision, life insurance, and disability benefits.

To develop this budget effectively, follow the 5 steps. First, assess your minimum legal requirements. Next, evaluate the cost ranges for group insurance. Then, choose a plan structure, such as a traditional insured plan, an HSA, or a hybrid option. After that, compile a total cost per employee, item by item. Finally, include renewal planning to ensure that the budget remains effective beyond the first year.

Additionally, how you structure the voluntary insurance offerings can impact your payroll tax exposure. The CRA considers employer-paid health and dental premiums as non-taxable benefits. In contrast, premiums for group life insurance, AD&D, and critical illness coverage are considered taxable benefits.

Once you understand these components, you will budget accurately for the true cost of your plan, not just the premiums.

What Influences the Costs of First-time Employee Benefits in Canada?

A Canadian first-time employee benefits budget consists of two components: the mandatory payroll obligations that every employer must fund, and the optional group insurance coverages that you choose to offer in addition.

Here are the key factors that impact your first-time benefit cost:

Mandatory Employer Costs

Before choosing any features for a group plan, ensure that your budget can cover mandatory costs, including CPP/QPP, EI, workers’ compensation insurance, the statutory vacation and sick leave mandated by federal and provincial laws. These costs are not optional, and failing to remit them accurately can lead to penalties and interest from the CRA.

The costs that employers can not skip are:

Canada Pension Plan/Quebec Pension Plan: Employers and employees each contribute 5.95% of pensionable earnings between $3,500 and the 2026 YMPE of $74,600, with a maximum contribution of $4,230.45 per person. Employers must match this amount. For earnings between $74,600 and $85,000, both contribute 4% (called CPP2), up to an additional $416 each. In Quebec, different rates apply under the QPP.

Employment Insurance: Many new employers often overlook this additional payroll cost. For the year 2026, employees pay $1.63 for every $100 of their earnings, up to a maximum of $68,900, resulting in an annual premium of $1,123.07. Employers will pay 1.4 times this amount, leading to a maximum cost of $1,572.30 per employee. In Quebec, employers need to consider a different rate for the QPIP.

Workers’ Compensation Insurance: In many jurisdictions, employers must register with the workers’ compensation board and pay premiums for workplace injuries and illnesses, which depend on the industry and past claims. Make sure to set aside a budget for this, as it’s different from group insurance premiums and payroll taxes.

Statutory Vacation and Sick Leave: Employers should comply with the employment rules in the jurisdictions where their employees work, as some leave types are unpaid, while others require employers to continue paying wages.

Voluntary Group Insurance Coverages

Once mandatory costs are covered, most budgeting decisions take place within the voluntary group insurance plan. A typical first group benefits plan includes a combination of extended health care, dental coverage, vision coverage, group life insurance, AD&D insurance, and disability insurance:

- Extended Health Care: This encompasses prescription drugs, paramedical services, medical equipment, and travel insurance.

- Dental Coverage: This includes preventive, basic, and major dental services, and may also cover orthodontics.

- Vision Coverage: This provides benefits for prescription eyewear and eye exams beyond what provincial plans cover.

- Group Life and Accidental Death & Dismemberment Coverage: This provides a lump-sum benefit to the employee’s beneficiary in the event of death or serious injury.

- Group Disability Insurance: This provides short-term and long-term income replacement for employees who are unable to work due to injury or illness.

Additionally, some employers offer group critical illness coverage, which provides a lump-sum payment upon the diagnosis of a covered condition, such as cancer or a stroke. The components you choose, along with the coverage levels for each, form your voluntary benefits budget.

How to Build Your First-time Employee Benefits Budget

To create a benefits budget as a first-time employer, follow five practical steps. First, conduct an audit of mandatory employer costs to establish a basic statutory floor. Next, evaluate the cost ranges for group insurance options. Then, choose a plan structure that fits within your budget. After that, compile a detailed line-item budget. Finally, incorporate renewal and cost-trend planning to ensure the budget remains effective beyond the first year.

By following this structured process, employers first-time setting up employee benefits in Canada can avoid common mistakes often made in the first year and provide a solid budget to present to their finance team or accountant.

The five steps outlined below explain the employee benefits budgeting process for first-timers in the correct order:

Step 1: Audit Your Mandatory Employer Costs

As mentioned, Canadian employers must calculate the statutory contributions they owe for each employee. Some provinces have additional employer payroll or health taxes on top of CPP and EI. Include these costs only if the province where your employee works has such taxes. These mandatory costs represent the minimum requirements for any employee benefits budget.

They are not fixed dollar amounts; instead, they increase with each new hire and every salary raise. This scaling effect is the reason why it is crucial to conduct a mandatory audit at the beginning of the budgeting process, rather than treating it as an afterthought.

Step 2: Understand What Group Insurance Costs in Canada

Group insurance premiums for Canadian employers vary widely, depending on several factors, including the plan’s richness, the workforce’s demographics, and the employer’s size. In Canada, most employers share the total premiums with their employees, typically on a 50/50 basis.

There is no single government-published benchmark for group insurance pricing. Rather, it is drawn from multiple Canadian benefits advisors and insurers and should be regarded as industry estimates rather than fixed rates.

For example, a team with an average age of 45 will pay more in premiums than a younger team because older employees tend to have higher medical claims.

Also, companies in high-risk industries, such as construction, face higher life and disability insurance premiums than those in lower-risk fields, such as professional services, even if they have the same number of employees.

Finally, a company’s claims history from the previous year affects its renewal premiums. This is why employee benefits premiums can differ between the first year, which is based on estimates, and the second year, which relies on actual claims data.

Step 3: Choose a Plan Structure That Fits Your Budget

Canadian employers commonly choose from three main group insurance structures: a traditional insured plan, an HSA, or a hybrid plan that combines both insured coverage and an HSA. Each of these options offers a different balance between predictable costs and employee flexibility.

The best choice depends on your budget’s tolerance for year-over-year changes and the level of choice you wish to provide employees regarding their coverage. Let’s look at the most common options:

Traditional Insured Plan

In this model, an employer purchases a group insurance policy from an insurer such as Sun Life, Manulife, or Canada Life. The carrier sets the premium rates, handles claims, and pays eligible expenses directly. Every year, during the renewal period, the company adjusts premiums based on the previous year’s claims.

This system provides comprehensive coverage managed by the insurer, but it can lead to unpredictable costs. A single high-cost claim, like a $30,000 specialty drug, can cause premiums to rise significantly at the next renewal, making it harder for employers to budget.

Health Spending Account

A Health Spending Account is a benefit where employers provide a fixed amount of money each year for employees to spend on eligible medical and dental expenses, as defined by the CRA.

This setup helps employers control costs and avoid surprises, such as sudden premium increases. HSAs are great for small businesses that want budget stability. However, a downside is that employees are responsible for covering any costs beyond their allocated amount, which might make them feel less secure compared to traditional insurance plans.

Hybrid Plan

This structure combines a basic, traditional insured plan that covers essential expenses like prescriptions and dental care at a lower coverage tier with an HSA for added flexibility. Employees are protected against common costs, but they also have HSA funds available for other important expenses, such as vision care or paramedical services.

This hybrid model is becoming popular among Canadian employers who want to attract talent without significantly increasing insurance costs. It allows employers to manage expenses effectively: they can control insurance premiums through plan elements like deductibles and coinsurance or copay, while the HSA is a fixed, manageable expense.

Step 4: Build a Line-Item Benefits Budget

A complete first-time budget for employee benefits is a document that combines mandatory statutory costs, group insurance premiums, taxable benefit surcharges, and administrative fees into a single annual total per employee. To create this budget, you will need to integrate the results from the previous three steps: the statutory minimum from Step 1, the premium estimates from Step 2, and the plan structure and cost-sharing arrangements from Step 3.

Example of creating a benefits budget with line items

Here is a simple example of an employee earning $60,000 per year in a province without an employer health tax. This example uses a standard insured plan in which the cost is split evenly between the employer and the employee:

| Line Item | Annual employer cost |

|---|---|

| CPP employer contribution (5.95% on $60,000 − $3,500) | $3,361.75 |

| EI employer premium ($60,000 × 1.63% × 1.4) | $1,369.20 |

| Workers’ compensation (illustrative: $1.50 per $100 of payroll) | $900.00 |

| Employer share of group premiums (50% of $300/month total) | $1,800.00 |

| Employer-paid group life/AD&D premium (taxable benefit) | $300.00 |

| Additional employer CPP on the taxable benefit (5.95% × $300) | $17.85 |

| Administration and pooling fees (illustrative) | $250.00 |

| Total annual employer cost | $7,998.80 |

Disclaimer: All group insurance numbers are examples; please use your actual quotes.

In this example, there are two main points to keep in mind. First, the required costs alone exceed $5,600 before adding any extra coverage; this amount is the “floor” from Step 1. Second, the taxable group life premium clearly affects things: it increases the employee’s pensionable earnings, which then raises your CPP payment. Use this template to make a spreadsheet, copy it for each employee (or salary group), and add up the numbers to find your total plan budget.

Step 5: Plan for Renewal and Year-Over-Year Cost Increases

Group insurance contracts usually renew every 12 months, and the premium changes upon renewal. Therefore, a benefits budget that only considers the first year of the contract will likely be inaccurate for the second year. Planning for renewal is essential; knowing how to budget for benefit rate increases transforms a one-time budgeting exercise into a sustainable, multi-year cost management strategy.

Insurers apply annual trend factors that account for expected increases in drug costs, utilization, and inflation. Based on your plan’s claims history, renewal premiums may increase by 5% to 15% or more. To manage your budget well, it’s a good idea to include a margin of at least 5% to 10% above your first year’s quoted premium when planning for the second year. By planning renewals this way, you can turn a one-time budgeting task into a long-term cost-management plan.

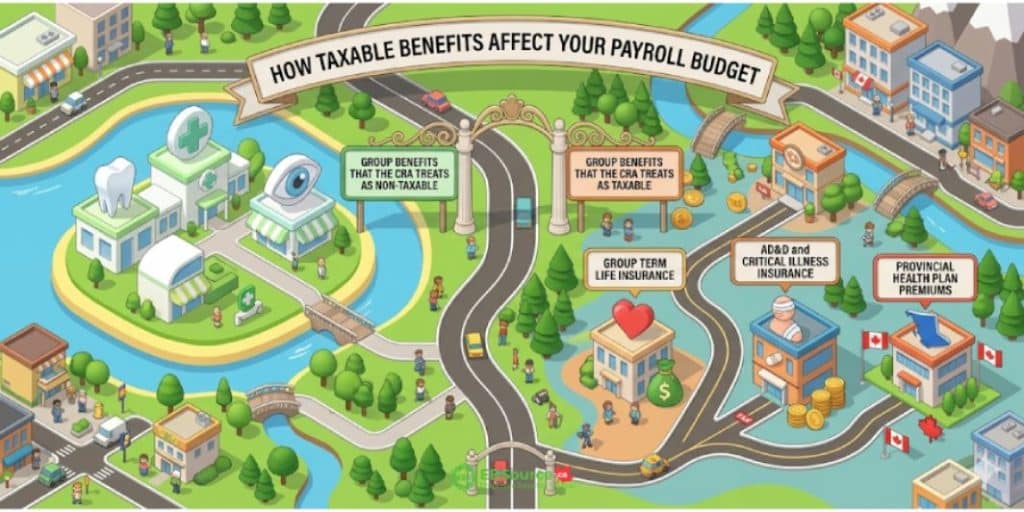

How Taxable Benefits Affect Your Payroll Budget for the First Time Setting Up Employee Benefits

Taxable benefits affect your payroll budget because the CRA treats employer-paid group benefits in two different ways: premiums for health, dental, and vision coverage under a private health services plan are non-taxable, while premiums for group term life, AD&D, and critical illness insurance are taxable benefits that must be reported on the employee’s T4 slip and included in CPP pensionable earnings. Misclassifying these benefits can inflate your payroll remittances or trigger CRA reporting errors in your first year.

The two categories below explain which benefits the CRA taxes, which it does not, and what each means for your payroll calculations, together with special rules for disability insurance:

Group Benefits that the CRA Treats as Non-taxable

Employer-paid premiums for a private health services plan (PHSP) are not considered a taxable benefit for employees. This includes the main components of most group plans, such as extended health care, dental, and vision coverage. If the plan meets CRA rules, meaning that 90% or more of the benefits provided are for expenses that qualify for the medical expense tax credit, the employer will not have to pay taxes on these employer contributions.

Group health and dental coverage is an efficient way to provide compensation because employers can deduct the premiums as a business expense, and employees receive the coverage without it counting as taxable income. If employees pay part of the premium, they may also qualify for a medical expense tax credit, further reducing costs.

Quebec note: Even if a benefit is not taxed by the federal government, Quebec may treat some employer-paid group insurance payments (including PHSP-type coverage) as taxable for Quebec income tax. Check Revenu Québec's instructions to find out how to report this on the RL-1 form.

Contributions to HSAs can also be treated as tax-free PHSP payments if set up correctly, providing employers with tax deductions and employees with tax-free reimbursements.

Group Benefits that the CRA Treats as Taxable

Three categories of employer-paid group benefits that commonly trigger taxable benefit rules are group term life insurance, AD&D and critical illness insurance, and provincial health plan premiums. Each of these affects your payroll calculations.

Group Term Life Insurance

The employer-paid premiums for a group term life insurance policy are considered a taxable benefit to the employee. As a result, you must include the value of these premiums in the employee’s income and report it on their T4 slip.

Since the premium payment is a non-cash benefit, it is counted toward CPP contributions but not toward EI. On the T4 slip, report the premium value in Box 14 (employment income), in Box 26 (CPP/QPP pensionable earnings), and again under Code 40 in the “Other information” area of the slip. Both the employer and employee contribute to CPP based on this amount, but you do not need to deduct EI premiums for this benefit.

AD&D and Critical Illness Insurance

AD&D and group critical illness insurance receive the same tax treatment as group life insurance. When employers pay premiums for group insurance plans that provide a lump-sum benefit (instead of periodic income replacement), these premiums are classified as a taxable benefit under paragraph 6(1)(e.1) of the Income Tax Act.

The amount of the premiums must be reported on the employee’s T4 slip, including under Code 40. As with group life insurance, the benefit is CPP-pensionable but not EI-insurable.

Provincial Health Plan Premiums

In some provinces, if employers pay health insurance premiums for their employees, these payments might be considered taxable benefits. This is less common now, as most provinces use payroll tax-funded models, but it can still occur in certain cases. So check the CRA benefits and allowances chart for your province’s current rules.

The Special Rule for Disability Insurance Premiums

Group disability insurance, covering both short-term and long-term periods, has a rule that can surprise new employers. Although employer-paid premiums for a group disability plan are not taxed as employee benefits when paid, any part of the premium paid by the employer means that disability benefits received later will be taxed as income when a claim is made.

On the other hand, if employees pay all disability premiums with pre-tax income, the benefits they receive during a disability are not taxed. Because disability benefits usually replace only 60% to 70% of an employee’s earnings before disability, taxing these benefits can leave disabled employees with much less money to live on during a difficult time.

Because of this, EBSource’s benefits advisors suggest setting up the plan so that employees pay the full disability premium, even if the employer pays for most or all other coverages. Keep this in mind when deciding how to share costs in Step 3, and make sure your payroll deductions and plan documents clearly show who pays the premiums.

What Mistakes to Avoid When Budgeting for Employee Benefits for the First Time?

The three most common mistakes first-time employers make when budgeting for employee benefits are underestimating the total cost beyond base premiums, ignoring renewal trend assumptions that can raise premiums by 5% to 15% at renewal, and failing to communicate the plan’s value to employees. Each mistake either understates your true annual cost or reduces the return you get from the plan.

Below are the ways these mistakes can lead to a wrong decision when budgeting employee benefits:

Underestimating Costs: Many new plan sponsors make the mistake of budgeting solely for base premiums. However, there are additional expenses to consider, including administration fees, pooling charges (which cover high-cost claims that exceed a specified threshold), and applicable provincial premium taxes.

Ignoring Renewal Trend Assumptions: As covered in Step 5, insurers apply annual trend factors for drug costs, utilization, and inflation, and renewal premiums can rise by 5% to 15% or more. Employers who skip the claims fluctuation margin recommended in Step 5 often face an unbudgeted shortfall in year two.

Ineffective Communication of Plan Value: Failing to communicate the plan’s value to employees can diminish its retention effectiveness. If employees do not understand what their plan covers or how to use it, they may undervalue the benefits. This can ultimately result in a loss of returns on the employer’s recruitment and retention investment.

By being aware of these pitfalls, first-time employers can make more informed decisions and create a more effective employee benefits strategy.

FAQs about How To Budget for Employee Benefits for the First Time

Can I start a group benefits plan if my company has fewer than three employees?

Yes, you can get group insurance, but it depends on the insurer. Most Canadian providers require at least 2 or 3 eligible employees to set up a traditional plan. However, some, such as the Chambers of Commerce Group Insurance Plan, offer plans for one or two employees. Typically, eligible employees must work 20 to 30 hours a week and live in Canada. If your team is too small for a traditional plan, an HSA is a good alternative with no minimum size requirements.

Should I hire a benefits broker, and how are they compensated?

A licensed benefits broker can help you create a benefits plan, get competitive quotes from different insurance companies, and manage the plan during renewals and claims. Brokers typically earn commissions from the insurance company, not directly from you, so using one usually does not raise your costs compared to dealing with an insurer yourself. Some may also charge fees for their services. It’s important to ask any potential broker how they’re paid upfront.

Are budgeting resources provided by employee benefits plans?

Most insurance companies and benefits brokers will give you budgeting tools like price lists, renewal cost estimates, and online cost calculators when you start a group insurance plan. Some insurers also share yearly comparison data so you can see how your plan’s costs compare to others in your field. If your provider does not offer these tools, a licensed benefits broker can usually get them for you for free, since brokers are paid by the insurers.

Article sources

Disclaimer: This guide serves as a planning resource and does not provide legal, tax, or payroll advice. Employer obligations in Canada vary based on the employee’s work location, whether the employer is federally regulated, and the applicable tax year or effective date. Before relying on any number or rule mentioned in this article, please verify it with the relevant authorities, such as the CRA or federal or provincial agencies.