Many plan members in group benefits plans are surprised when their health or dental claim is reimbursed at a lower amount than expected. In most cases, the reason is something called a Reasonable and Customary (R&C) limit.

Reasonable and Customary (R&C) limits are the maximum amounts an insurer will reimburse for a service, based on typical costs in your area. If your provider’s fee is higher than that ceiling, your plan’s coinsurance is applied only to the capped amount. This leaves you to pay not only your usual share but also the entire difference that went over the limit.

These limits most often affect services with variable pricing, such as paramedical and dental services, prescription drugs, and medical equipment. To control costs, you can check your R&C limits before treatment, confirm fees with your provider, and request a pre-determination for larger expenses to know exactly what your plan will cover.

What Are Reasonable and Customary Limits?

Reasonable and Customary (R&C) limits are the maximum amounts an insurance provider considers eligible for reimbursement under a group benefits plan.

Instead of automatically covering the full amount charged by a clinic or practitioner, insurers compare the fee against the typical cost of the same service in your province or region. If a provider charges more than the R&C limit, you may need to pay the difference out of pocket.

R&C limits can be different across Canada because health care and paramedical service fees vary by province or territory. Additionally, each insurance company has its own way of calculating these limits, so the R&C amounts for the same service can differ between companies.

These limits are reviewed and updated periodically to reflect changes in market pricing. Since reimbursement limits may change over time, it is important to check your coverage before starting treatment or visiting a new provider.

How Your Claim Is Calculated When Fees Exceed R&C

When a provider charges above the Reasonable & Customary (R&C) limit, the insurer reimburses only up to the approved R&C amount, and you pay the rest. In most cases, the claim calculation follows a step-by-step process, starting with setting the R&C amount, applying coinsurance, and leaving the rest to you.

Here is how the claim is usually calculated step by step:

- Step 1: The insurer identifies the R&C limit for the specific service or product in your province or territory. If the provider’s charge is higher than that limit, the eligible amount is capped at R&C.

- Step 2: The plan applies its coinsurance percentage to the R&C amount established for that service.

- Step 3: You pay any remaining balance, including both your normal coinsurance share and any amount charged above the R&C limit.

The insurer does not split the overage with you or apply coinsurance to it; that portion is entirely your responsibility.

The following table uses hypothetical figures (based on a $100 R&C limit and 80% coinsurance) to show how a single paramedical visit produces different out-of-pocket results depending on whether the provider charges within or above R&C.

| Charge Within R&C | Charge Above R&C | |

| Provider’s charge | $90.00 | $130.00 |

| Plan reimburses (80% of the eligible amount) | $72.00 | $80.00 |

| Your out-of-pocket cost | $18.00 | $50.00 |

When the provider charges above R&C, the member’s out-of-pocket cost nearly triples in this scenario, even though the plan’s reimbursement increases by only $8.00.

In both cases, the plan applies the same 80% coinsurance rate. The difference is entirely driven by where the provider’s fee falls relative to the R&C limit.

- When the charge is within R&C, the insurer considers the full charge eligible, and you pay only your coinsurance share.

- When the charge exceeds R&C, the $30.00 overage in the right column falls entirely on you, added on top of your $20.00 coinsurance share of the $100.00 R&C amount.

Smart shopping for health care services and products can help lower your out-of-pocket costs. Confirming your provider’s fees against your plan’s R&C schedule before booking is the most reliable way to avoid this additional cost.

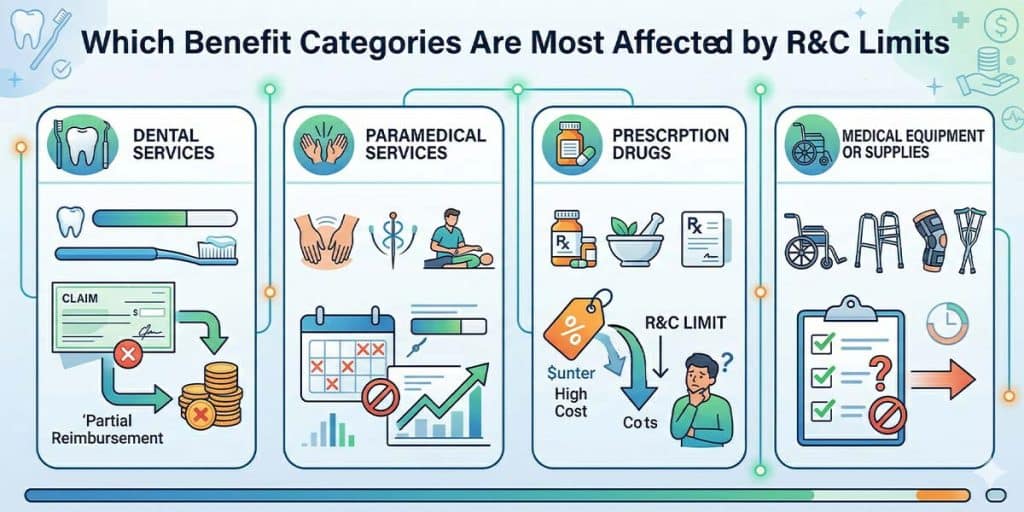

Which Benefit Categories Are Most Affected by R&C Limits

Dental services, paramedical services, prescription drugs, and medical equipment or supplies are the benefit categories most commonly affected by R&C limits.

The table below summarizes, by benefit category, how the R&C reference is established and why a provider’s fee may end up above that ceiling.

| Benefit Category | How the R&C Reference Is Set | Why Provider Fees May Exceed the R&C |

| Dental services | Provincial dental association annual fee guides (e.g., guidelines published by the Ontario Dental Association) | A dentist may bill above the published guide rate |

| Paramedical services | Insurer underwriting guidelines; no standardized provincial schedule | No regulated fee schedule; clinic pricing varies widely |

| Prescription drugs | Provincial government drug plan rules and insurer pharmacy benefits manager | Each pharmacy sets its own markup and dispensing fee |

| Medical equipment or supplies | Insurer underwriting; no standardized public price list | No regulated retail price guide; supplier pricing varies |

Dental benefits

Dental services are typically more predictable because insurers base R&C limits on provincial dental association fee guides. If a dentist charges close to the guide rate, your claim usually falls within the R&C limit. However, dentists are not required to follow these guides, and billing above the published rates can still create a gap.

Example: You receive a root canal treatment in Quebec in 2026. The Association des Chirurgiens Dentistes du Québec (ACDQ) fee guide lists approximately $749 for this procedure (code 3310). Some insurers may use provincial dental fee guides as one reference point when determining Reasonable and Customary (R&C) limits, although reimbursement limits can vary by insurer, region, and plan design. In this hypothetical example, assume your insurer uses an R&C limit of $749, and your dental plan includes 80% coinsurance.

The following table shows how your costs change when a dentist charges above the recommended fee guide:

| Expense | Dentist Charges Fee Guide | Dentist Charges Above Fee Guide |

| Dentist’s Fee | $749 | $850 |

| R&C Limit | $749 | $749 |

| Eligible Amount | $749 | $749 (Capped) |

| Insurer Pays (80%) | $599 | $599 |

| You Pay | $150 | $251 ($150 coinsurance + $101 over R&C) |

Even if the dentist charges $850, the insurer still only calculates coinsurance on $749. The $101 portion exceeding the R&C limit is entirely your responsibility. The portion exceeding the R&C limit becomes your responsibility in addition to your normal coinsurance share.

Paramedical services

Paramedical services often create larger R&C gaps because pricing can vary significantly between clinics and practitioners. Unlike dental services, many paramedical categories do not follow standardized provincial fee schedules. This category may include chiropractors, massage therapists, physiotherapists, counsellors, psychotherapists, and naturopaths.

For example, assume a group benefits plan applies a 2026 R&C limit of $160 for a 60-minute massage therapy session in British Columbia, with 80% coinsurance.

The table below shows how out-of-pocket costs can differ when providers charge different fees for the same type of service.

| Clinic A (Suburban) | Clinic B (High-end Downtown) | |

| Massage Fee | $155 | $210 |

| R&C Limit | $160 | $160 |

| Eligible Amount | $155 | $160 (capped) |

| Insurer Pays (80%) | $124 | $128 |

| Out-of-Pocket Cost | $31 | $82 ($32 coinsurance + $50 over R&C) |

If you go 10 times per year:

- Clinic A: Total out-of-pocket = $310/year

- Clinic B: Total out-of-pocket = $820/year

Two clinics in the same city can vary in price, but the insurer will only pay what it deems reasonable, which is why paramedical services carry the highest gap risk.

Prescription drugs

Prescription drug claims can also be affected by R&C limits because the total cost includes multiple components, such as the drug ingredient cost, pharmacy markup, and dispensing fee. Since pharmacies may set different markups and dispensing fees within provincial rules, the total billed amount can vary between locations.

For example, suppose you fill the same prescription at two different pharmacies in British Columbia. Your insurer sets an R&C Dispensing Fee Limit of $11.00 for this specific prescription, with an 80% coinsurance plan.

This breakdown shows how R&C dispensing fee caps impact your total out-of-pocket expense:

| Cost Breakdown | Pharmacy A | Pharmacy B |

| Drug Ingredient Cost | $20.00 | $20.00 |

| Pharmacy Markup (typically ~8–10%) | $1.60 | $2.00 |

| Dispensing Fee | $8.00 | $14.99 |

| R&C Dispensing Fee Limit | $11.00 | $11.00 |

| Eligible Dispensing Fee Amount | $8.00 | $11.00 (capped) |

| Insurer Pays (80% of the eligible dispensing fee) | $6.40 | $8.80 |

| Employee Coinsurance on Eligible Amount (20%) | $1.60 | $6.19 ($2.20 coinsurance + $3.99 over R&C) |

| Total Out-of-Pocket Cost | $23.20 | $28.19 |

The gap here is smaller compared to paramedical services, but it becomes significant when accumulated over multiple refills throughout the year. If you refill this prescription monthly (12 times/year), the difference is approximately $60/year for just one medication. For individuals taking multiple chronic medications, this difference can easily scale to hundreds of dollars per year.

Medical equipment or supplies

Medical equipment and supplies present similar challenges. These items usually do not have a standardized public price list, and suppliers may charge above typical market rates. Insurers therefore rely on internal benchmarks, which can lead to gaps between billed prices and R&C limits.

For illustrative purposes only, assume a group benefits plan provides coverage for orthopedic shoes in British Columbia with an annual maximum benefit of $400 per person per calendar year and an 80% coinsurance rate. In practice, members may need to confirm eligibility and approval requirements with their insurer before purchase.

The following table compares your out-of-pocket costs when purchasing from two suppliers with different pricing.

| Supplier A | Supplier B | |

| Retail Price | $375 | $550 |

| R&C Limit | $400 | $400 |

| Eligible Amount | $375 | $400 (capped) |

| Insurer Pays (80%) | $300 | $320 |

| Out-of-Pocket Cost | $75 | $230 ($80 coinsurance + $150 over R&C) |

Pro tip: Because paramedical services and medical equipment lack consistent pricing benchmarks, they tend to produce the largest R&C gaps. Checking your plan’s limits before booking these services can help you better estimate your out-of-pocket costs.

How to Control Your Out-of-Pocket Costs

You can often reduce out-of-pocket expenses by checking your plan’s R&C limits, confirming provider fees in advance, comparing pharmacy pricing, requesting pre-determinations for larger claims, and reviewing itemized receipts carefully. Taking these steps before treatment can help you better understand your coverage, avoid unexpected claim gaps, and maximize your reimbursement.

Here are five practical steps you can take to maximize your benefits and protect your wallet:

- Check your limits online: Most insurers allow members to review current R&C limits through their online benefits portal or customer support services.

- Ask your provider: Once you know your R&C limit, ask your practitioner if their fees fall within that amount.

- Shop around for prescriptions: Pharmacy dispensing fees can differ a lot, even in the same area. To save money, check prices at more than one pharmacy. If you need ongoing medications, ask for a bigger supply. This way, you can pay fewer dispensing fees throughout the year.

- Request a pre-determination: For larger expenses, such as medical equipment, specialty treatments, or major dental work, submit an estimate to your insurer beforehand to ensure you know exactly how much the plan will reimburse and what your personal financial responsibility will be.

- Review itemized receipts: Requesting a detailed breakdown of charges from clinics or pharmacies helps you identify exactly which components of a bill exceeded your plan’s reimbursement limits.

Taking these steps before treatment can help reduce unexpected claim gaps and out-of-pocket expenses.

Why R&C Limits Exist in Group Benefits Plans

R&C limits help control overall claim costs, support the plan’s sustainability for all members, and reduce the risk of fraud and abuse. Because group benefits plans are shared pools of funding, the actions of a few can impact everyone. Here is why these limits are essential:

Controlling Costs

When any provider charges well above typical market rates, the higher cost pressures the entire plan. R&C limits are important to ensure claims to your benefits plan are not excessive, which helps stabilize costs for everyone covered under the plan.

Protecting Plan Sustainability

Insurers view R&C as a way to share responsibility. The plan pays for the fair market cost of a service. By helping to keep claim costs reasonable, you help protect the long-term health of your benefits plan.

Preventing Fraud and Abuse

R&C limits help reduce the risk of unreasonable or inflated claims by setting reimbursement amounts based on typical regional pricing. Without these limits, providers could charge significantly more than standard market rates, increasing costs for the entire benefits plan.

These safeguards also help insurers identify unusual billing patterns, such as charges that are consistently higher than what most practitioners in the area charge for the same service. By limiting reimbursements to reasonable amounts, R&C limits discourage excessive billing and help protect plan funds for all members.

Edge Cases and Plan Features That Interact With R&C Limits

Some features of your plan and different situations can affect how Reasonable and Customary (R&C) limits apply to your claim. For instance, how much you get reimbursed might change if you receive treatment in another province, if there are annual or specific limits for certain practitioners, or if you use a Health Spending Account (HSA) to pay for costs above the R&C limit.

Knowing these situations can help you estimate your out-of-pocket expenses more accurately.

When your service provider is located in a different province from where you live

In many plans, the R&C limit is based on the location where the service is performed, not where you live. If you receive care in another province, the applicable R&C limit reflects the typical cost in that region.

Because healthcare pricing varies across provinces, this can result in higher or lower reimbursement compared to receiving the same service in your home province.

How annual benefit maximums and per-practitioner limits interact with R&C limits

R&C limits apply at the claim level, while annual maximums and per-practitioner limits apply at the plan level. Both can affect your reimbursement.

For example, if your provider charges above the R&C limit, the insurer first caps the eligible amount. Then, the reimbursed portion is applied against your annual maximum or practitioner-specific limit. Once you reach these limits, no further reimbursement is available, even if future claims fall within the R&C range.

Using a Health Spending Account (HSA) to cover R&C gaps

If your benefits package includes a Health Spending Account (HSA), you may be able to use it to cover costs not reimbursed by your group plan, including amounts above the R&C limit.

An HSA allows you to claim eligible medical expenses using employer-funded credits. While it does not change your plan’s R&C limits or co-insurance, it can reduce your out-of-pocket cost by covering the remaining balance.

FAQs

Do R&C limits reset at the start of each benefit year?

No. R&C limits are not a budget that changes each year. They are a price cap set by your insurance company based on local market rates. These limits stay in place until the insurance company decides to change them, which can happen at any time.

If my provider gives me a discounted rate, does my insurer reimburse based on what I paid or the published R&C amount?

Insurers usually pay back the lower amount between what you were charged and the R&C limit. If your provider gives you a discounted rate below the R&C limit, your reimbursement will be based on what you actually paid. Keep your receipt, as insurers may ask for proof of the amount you paid.

Are R&C limits the same thing as the annual benefit maximum on my plan?

No. R&C limits apply to each individual service, while the annual benefit maximum is the total amount your plan will pay for a category over the year. Even if you have unused annual coverage, each claim is still capped by the R&C limit.

Can my employer negotiate or adjust R&C limits when setting up a group benefits plan?

No. R&C limits are set by the insurer based on market data and are not typically adjustable by the employer. However, employers may offer a Health Spending Account (HSA), which can help cover costs that exceed plan limits.

If I coordinate benefits with my spouse’s plan, does the second insurer apply its own R&C limits?

Yes. When you coordinate benefits between two group health plans, each insurer looks at its own allowed amounts separately. The total payment from both plans cannot exceed 100% of your actual medical expense, and neither plan will pay more than its own allowed amount for the service.