In Canadian group benefits, a late applicant is any employee or dependant who enrols in the plan more than 31 days after becoming eligible. Missing that window can result in dental dollar caps, delayed coverage or outright denial of benefits. This risk is specific to group insurance plans (health, dental, life, and disability) and does not apply to other benefits that have their own enrolment rules, such as Group RRSPs or Health Spending Accounts.

However, late applicant status can be avoided through timely onboarding, proper use of life-event triggers, and clear communication between the plan administrator and each eligible employee.

What is a Late Applicant in Group Benefits?

A late applicant is any person who enrols in a group benefits plan more than 31 days after their eligibility date. This rule applies equally to new employees and to their dependents, such as a new spouse or child.

For example, if an employee marries but does not add the spouse to the plan within 31 days of the wedding date, the spouse is considered a late applicant. The same principle applies to adding a newborn, an adopted child, or a common-law partner who has met the cohabitation requirement.

Why does the 31-day rule exist?

Insurers set premium rates on the assumption that all eligible members will join, which spreads financial risk across healthy and less healthy individuals. The 31-day rule exists to prevent employees from only joining the plan when they need expensive care, which causes a significant rise in claims and higher premiums for every plan member.

When Does the 31-Day Enrolment Window Start?

The single biggest reason employees accidentally become late applicants is confusing their hire date with their eligibility date. The 31-day enrolment window begins on the employee’s eligibility date, not their hire date. The eligibility date is the day the benefits plan officially begins, which comes after any employer-mandated waiting period.

To better understand how this timeline works in practice, consider the following example for a new hire:

- Employment Hire Date: June 1

- Waiting Period: 3 months

- Eligibility Date: September 1

- Benefits Registration Deadline: October 1 (31 days after the September 1 eligibility date)

In this case, an employee who enrols after October 1 is a late applicant. To prevent this, many insurers allow employees to complete and submit their enrolment forms during the waiting period, even though coverage will not start until the eligibility date.

For dependants being added due to a life event, the 31-day window starts on the date of the event itself:

- The new spouse must be enrolled within 31 days of the marriage date.

- A newborn or newly adopted child must be enrolled within 31 days of the date of birth or adoption.

- A common-law partner becomes eligible after a set period of cohabitation, typically 12 months, though this can vary by insurer. After that, the 31-day window begins.

Important note: The deadline applies to when the insurer receives the completed enrolment form, not when the employee completes it. A form completed on time but submitted late by the plan administrator will still result in late applicant status.

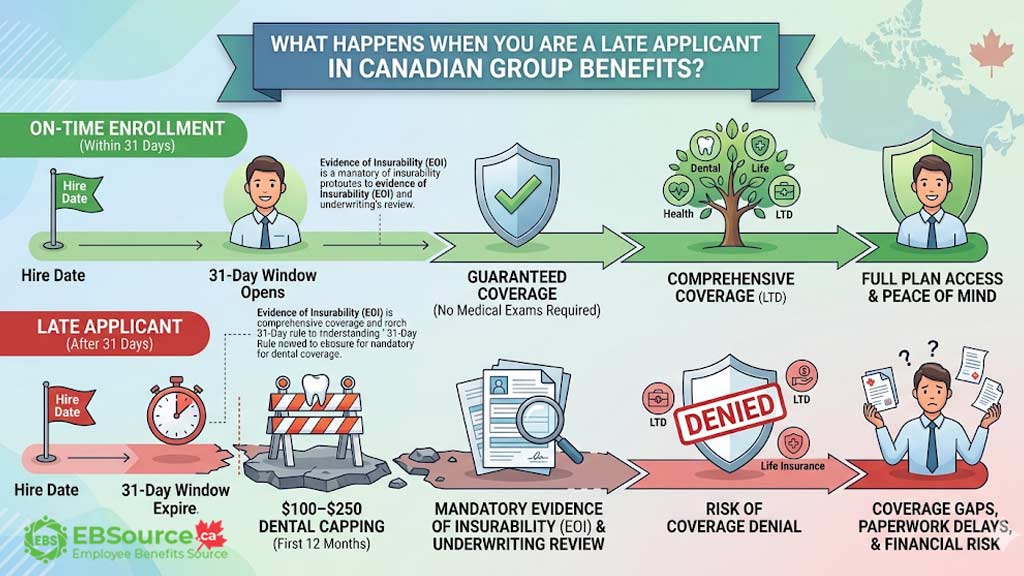

What Happens When You Are a Late Applicant?

When you (or your dependant) are flagged as a late applicant, your status changes from “guaranteed” to “conditional.” Missing the enrolment deadline can lead to three major consequences: losing automatic approval, facing a possible denial of benefits, and being subject to coverage restrictions or limitations.

The three major consequences are:

Loss of Automatic Approval

Missing the enrolment deadline means that you lose the right to automatic approval and must provide Evidence of Insurability (EOI). EOI is the process by which an insurer assesses an individual’s health to determine if they are eligible for coverage.

Depending on your health history, the insurer may request blood tests, medical exams, or attending physician statements (APS), and you are responsible for any associated costs.

Outright Denial of Benefits

The insurer’s review of the EOI application can lead to one of three outcomes: full approval, approval with restrictions, or outright denial.

- Approved: The applicant is granted coverage.

- Approved with Restrictions: The applicant is granted coverage but with specific restrictions, such as a cap on dental benefits.

- Denial: The insurer denies the application for coverage, and the individual is excluded from that part of the benefits plan.

During the review period, you have zero active coverage. If approved, coverage begins on the insurer’s approval date, not the original eligibility date, creating a potential coverage gap. During that gap, the employee is fully exposed and here is what could happen:

- If the employee is diagnosed with a serious illness during weeks 2–4 of the review, the diagnosis becomes a pre-existing condition that the insurer may use to deny the application entirely.

- If the employee needs emergency dental work during the review period, none of it is covered.

- If the employee dies during the review period, the life insurance benefit has not yet been approved, meaning no payout to their beneficiaries.

Coverage Restrictions

Even if you are eventually approved, you will face significant delays and limitations that do not apply to on-time applicants. Some consequences are temporary while others are permanent.

The most common penalty is a restriction on dental benefits. Many insurers will cap dental reimbursements at a low amount (e.g., $100-$250 per person) for the first 12 months of coverage. That sounds like a minor inconvenience, until you look at what dental work actually costs in Canada.

According to Canada Life, the average cost for a dental crown in Canada is between $900 and $1,500 (Source). In Ontario specifically, dental crown costs typically range between $800 and $2,000 (Source).

The following example table shows how a late applicant dental cap can significantly increase out-of-pocket costs compared to a regular plan member with standard coverage:

| Regular Plan Member (80% coverage) | Late Applicant ($250 cap) | |

| Crown cost | $1,200 | $1,200 |

| Insurance pays | $960 | $250 |

| You pay out of pocket | $240 | $950 |

In this example, the late applicant pays approximately $700 more out of pocket for a single dental procedure. The financial impact can become even more significant if additional treatment is required. For example, a root canal combined with a crown can cost between $2,000 and $3,500. Under a late applicant restriction, only $250 of that total would be covered for the entire year.

For health, life, and disability insurance, the biggest risk is an outright denial of coverage. An employee who applies on time receives these benefits without providing medical proof, while a late applicant loses this guarantee. In addition, employees cannot retroactively restore coverage that has been denied. If an insurer denies an application for LTD coverage, for example, you will lose access to a crucial financial safety net that could have replaced a significant portion of your income during an illness or injury.

The table below summarizes the most common restrictions across four core benefit categories:

| Benefit Type | Typical Late Applicant Restriction | Duration |

| Health (extended health care) | EOI required; if approved, effective date is the insurer’s approval date, not the original eligibility date | Gap from eligibility date to approval date |

| Dental | Per-person dollar cap of $100 to $250 | First 12 months of coverage |

| Life and AD&D | EOI required; denial possible for high coverage amounts or pre-existing conditions | Permanent if denied; standard coverage resumes after approval |

| Long-term disability (LTD) | EOI required; denial is most common for applicants with pre-existing conditions | Permanent if denied |

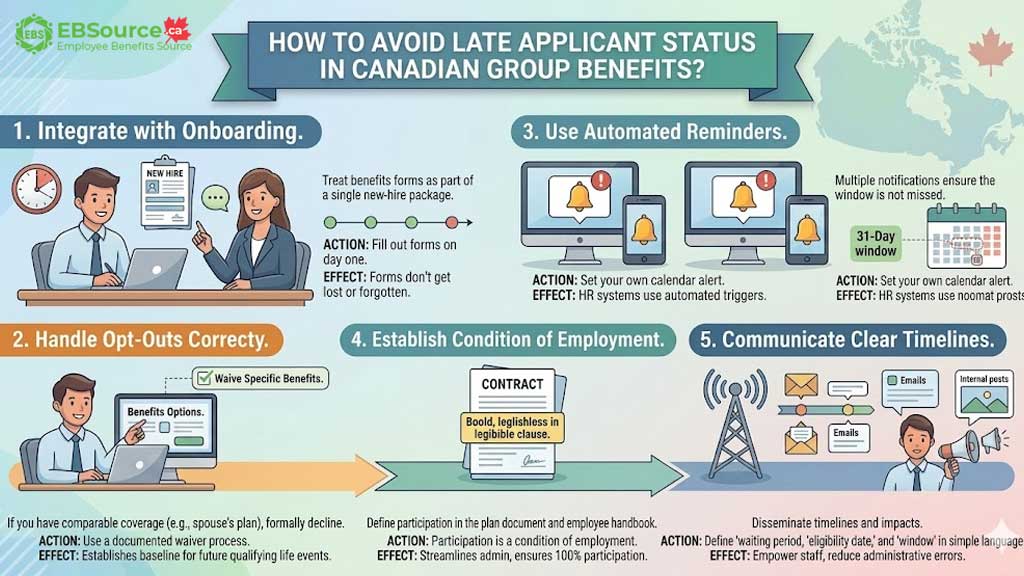

How to Avoid Late Applicant Status

Late applicant status is almost always preventable with five proactive practices: enroll during onboarding, waive coverage, set reminders, make enrollment mandatory, and communicate clearly.

These practices help protect both employees and employers:

- Enrol During Onboarding: Include benefits enrolment as a standard part of the new-hire process. The forms can be completed on the first day and submitted by the plan administrator upon the end of the waiting period.

- Formally Waive Coverage: If you do not need coverage (for example, you are covered under your spouse’s plan), do not simply ignore the enrolment forms. Formally complete the waiver section of the enrolment form within the 31-day window to preserve your right to join the plan later without being considered a late applicant.

- Set Calendar Reminders: Plan administrators should use a reminder system to track every new employee’s 31-day enrolment deadline.

- Make Enrolment Mandatory: Many employers require participation in the benefits plan as a condition of employment. This simplifies administration and ensures no one misses the window.

- Communicate Clearly: Employers need to educate employees on the consequences of missing the enrolment deadline and the importance of reporting life events in a timely manner.

What to Do If You Are Already a Late Applicant?

Late applicant status is not a permanent dead end, but resolving it requires quick action to minimize your risk. These may include contacting your plan administrator or benefits advisor to discuss making retroactive premium payments, submitting an Evidence of Insurability (EOI) or waiting for a plan renewal/insurer switch.

Here is how each option works:

- Explore Back-Pay Premiums: Some insurers allow employers to pay the missed premiums retroactively from the original eligibility date. If this option is permitted, the employee can be enrolled without providing an EOI. However, this is not a universal policy, and employers must confirm with their insurer if it is allowed and how far back they can pay.

- Submit the EOI Promptly: If back-paying premiums is not an option, you must complete the EOI process immediately to minimize any further delay in obtaining coverage.

- Wait for an Insurer Switch: When a company changes its benefits provider, the new insurer often allows all employees to enrol without late applicant restrictions, offering a fresh start.

Important: Never attempt to falsify hire dates or life event dates to appear on time. This is considered fraud and can lead to the denial of future claims and potential termination of the entire group plan.

FAQs about Late Applicant in Group Benefits

Do I have to pay out of pocket for medical tests requested during the EOI process?

Yes. If the insurance underwriter requires additional details, blood work or specific physician reports to assess your late application, you are strictly responsible for paying any associated costs.

Is it possible to appeal if an insurance carrier denies my late application?

Generally, no. If a carrier denies your coverage based on the medical evidence provided, there is rarely any recourse, and you will be excluded from that portion of the group plan for the year.

What happens if I miss the 31-day window because I was on vacation or medical leave?

The 31-day deadline is rigid and applies regardless of your personal schedule or approved leave. If you are absent when your eligibility window opens, you or your employer must still ensure the enrolment forms reach the insurer on time.