As your Small-Medium Businesses (SMEs) grow, the group benefits plan that once worked for a small team can quickly become expensive, difficult to manage, and misaligned with employee expectations.

A scalable group benefits plan allows your business to gradually expand coverage while keeping costs predictable and management easy. You can develop a flexible plan that grows with your company instead of having to rebuild it every few years.

This guide outlines six practical steps Canadian SMEs can use to build a scalable employee benefits plan. It covers how to assess workforce needs, create a flexible coverage structure, manage long-term costs, streamline administration, communicate benefits effectively, and prepare for annual renewals as the business grows.

Step 1: Assess Your Workforce Needs

To build a sustainable plan, growing SMEs must balance corporate financial metrics with genuine employee needs.

To avoid guessing as headcount scales, you must establish a data-driven baseline by calculating your Cost Per Employee Per Year (CPEY) to measure current efficiency, modelling a 3-year benefits budget to forecast future liabilities, and conducting a 5-question pulse survey to identify what your workforce truly values.

Calculate Your Cost Per Employee Per Year (CPEY)

To understand your current benefits efficiency, calculate your per-employee cost using this formula:

Benefits Cost Per Employee = Total Annual Benefits Spend ÷ Average Number of Employees (Source)

Example: If your company’s total contribution to the annual premium is $24,000 for 10 covered employees, your Annual Benefits Cost Per Employee is $2,400 (or $200 per month).

Many business owners mistakenly assume this cost scales linearly, calculating that growing to 50 employees will simply increase their budget to $120,000.

However, as your workforce grows, increased healthcare utilization and large claims can drive your actual cost per employee up to $3,200 or more. Without a properly structured plan, your real budget could spike to $160,000. This creates an unbudgeted $40,000 financial gap that directly erodes your profit margins.

Model Your 3-Year Benefits Budget.

Map out your hiring forecast for the next 12, 24, and 36 months. Create a spreadsheet using the template below to model future liabilities:

| Metrics | Year 1 (Current) | Year 2 (Projected) | Year 3 (Projected) |

| Projected Headcount | 12 | 25 | 50 |

| Target CPEY (Max Cap) | $2,200 | $2,200 | $2,200 |

| Total Projected Budget | $26,400 | $55,000 | $110,000 |

| Traditional Renewal Buffer (15%) | $3,960 | $8,250 | $16,500 |

Conduct a 5-Question Pulse Survey

Do not guess what your employees want. Set up a simple, anonymous survey using Google Forms or Typeform. Send it to your team with these exact questions:

- Which benefits matter most to you? (Rank in order: Prescription Drugs, Dental Care, Mental Health, Vision, Paramedical/Massage).

- Do you have alternative health coverage through a spouse’s or partner’s plan? (Yes / No).

- What healthcare services do you regularly pay for completely out of pocket? (Open text).

- Would you prefer a fixed benefit package (example: 80% drug/dental coverage) or a customizable spending account where you choose how to spend a set annual dollar amount?

- How important is virtual healthcare/telemedicine access to you on a scale of 1 to 5?

Pro Tip: Run this survey exactly $90 days before your policy renewal date. It provides your benefits advisor with the quantitative data needed to renegotiate design options with carriers.

Step 2: Build a Modular Benefits Plan That Scales With Your Business

A modular benefits plan allows employers to expand coverage as the business grows instead of redesigning the plan from scratch.

To build this flexibility, you must establish a structural foundation by building your benefits budget for future growth, choosing a contribution strategy that remains sustainable over time, starting with core coverage and expanding gradually as your business matures, and selecting an insurance carrier that supports future plan changes seamlessly.

Build Your Benefits Budget for Future Growth

A plan that feels affordable for a team of 10 can become financially unsustainable when you scale to 50.

When setting a benefits budget, employers should consider both current affordability and future sustainability. Leaving room for future enhancements can make it easier to add coverage later without requiring major changes to the plan structure.

To build a sustainable budget, apply the buffer strategy. Instead of spending your absolute maximum budget immediately, design a plan that leaves a 15% to 20% financial buffer per employee.

Example: If your company determines it can afford to spend CAD 2,500 per employee annually, do not buy a plan that costs CAD 2,500. Instead, design a foundational plan that costs CAD 2,000.

Leaving this CAD 500 buffer accomplishes two critical things as you grow:

- It absorbs inflation: Insurance premiums naturally rise over time due to inflation and team usage. Your buffer allows you to absorb these annual increases without being forced to downgrade coverage or suddenly ask employees to pay more out of pocket.

- It funds future upgrades: As your workforce matures, they will ask for better perks. Your built-in buffer gives you the financial room to introduce exciting new coverage, like a Health Spending Account (HSA) or enhanced mental health support, as a strategic reward when the company hits its growth milestones.

By leaving room in the budget today, you make it infinitely easier to scale your coverage tomorrow without requiring major, disruptive changes to the plan’s structure.

Choose a Contribution Strategy That Remains Sustainable

Before launching a plan, you must decide exactly how the monthly insurance bill will be split between the company and your employees.

Many SMEs use a cost-sharing model in which the employer covers a portion of the premium while employees contribute the remainder through payroll deductions. Establishing a contribution strategy early can help create predictable budgeting and reduce the need for significant changes as the workforce grows.

Common Contribution Splits for Canadian SMEs:

- 50/50 Split: The basic plan has the employer and employee sharing the total monthly premium equally. This approach is very suitable for early-stage startups.

- 70/30 or 80/20 Split: The employer covers most of the costs, making the benefits package a strong tool for attracting new employees. At the same time, the employer shares some of the financial responsibility.

- 100% Employer-Paid: Highly attractive for talent, but the most dangerous for growing SMEs, as you absorb 100% of future premium increases.

Pro tip: Regardless of the overall percentage split you choose, you should structure your payroll deductions so that the employee pays 100% of the Long-Term Disability (LTD) and Short-Term Disability (STD) premiums.

Start With Core Coverage and Expand Gradually

A modular benefits plan is created in stages. Employers start with basic coverage and can add more benefits as their workforce needs and business priorities change.

The table below illustrates how many SMEs gradually expand their benefits offerings as the business matures:

| Business Stage | Recommended Coverage Priorities | Best Suited For | Strategic Goal |

| Foundation Plan | Prescription drugs, basic dental, group life insurance | SMEs launching their first plan or businesses with 3-5 employees | Establishes essential healthcare protection while keeping the plan simple and manageable |

| Expansion Plan | Paramedical services, mental health support, Employee Assistance Programs (EAPs), short-term and long-term disability insurance | Growing SMEs with more stable revenue and 5-15 employees | Improves employee support, productivity, and retention as workforce expectations increase |

| Retention Plan | Group RRSP matching, enhanced dental coverage, Health Spending Accounts (HSAs) | More established SMEs with 15+ employees or specialized talent needs | Strengthens long-term retention and improves competitiveness for experienced hires |

These stages should be viewed as a planning framework rather than a fixed roadmap. The timing of future enhancements should be based on workforce needs, business performance, and recruitment goals rather than employee count alone.

Select a Carrier That Supports Future Plan Changes

As organizations grow, employers may want to introduce new coverage options, add employee classes, increase coverage limits, or implement programs such as HSAs or EAPs.

Choosing a carrier that can handle changes makes it easier to update your plans in the future. A flexible plan structure can lower the need for major redesigns and help employers adjust their benefits strategy as their business needs change.

A scalable benefits plan is not built all at once. It is built through a series of deliberate decisions that allow coverage, costs, and administration to grow alongside the business.

Example: Consider TechFlow, a startup growing from 15 employees to 40 employees. Management decides to introduce a $500 Health Spending Account for all employees and enhance dental coverage for five senior managers.

- Scenario A: TechFlow cannot support Health Savings Accounts (HSAs) or multiple plan options, so the policy must be cancelled. HR spends over 30 hours on re-enrollment, which means employees receive new cards, and all mid-year dental and vision limits reset.

- Scenario B: TechFlow signs a one-page Plan Amendment. The HSA and Executive Class will automatically appear in the employees’ existing mobile app next week with zero team disruption.

To make sure your business has a smooth transition, check your potential carrier against these important scalability criteria:

- Multi-Class Flexibility: As organizations grow, their employee benefit needs can vary. Some insurance providers, like Sun Life and Canada Life, offer plans that accommodate different employee groups and coverage options.

- Modular Coverage Options: Employers may eventually want to add HSAs, virtual care, wellness accounts, or enhanced mental health support. Solutions such as Honeybee through Empire Life and Blendable are designed to make these additions easier.

- Renewal Stability: As companies grow, they often use more benefits. Some plans, like the Chambers Plan, share risk among a larger group of members. This can help smaller employers have more stable renewal rates.

Pro Tip: You can not create a benefits plan all at once. Instead, choose a carrier that offers easy upgrades. This way, your coverage, costs, and administration can grow smoothly as your business grows.

Step 3: Control Costs as Your Team Grows

A scalable group benefits plan should remain financially sustainable as headcount, utilization, and employee expectations evolve over time.

To maintain cost stability, SMEs should understand how their plan is funded, implement practical claims management strategies, and invest in preventative wellness support that reduces long-term risk.

Understand Your Funding Model: Pooled vs. Experience-Rated

Canadian insurers generally price group benefits using one of two risk-sharing models: pooled plans or experience-rated plans.

This table compares two models across critical decision-making criteria, including operational mechanics, business size suitability, premium rate stability, cost drivers, and long-term strategic focus:

| Feature | Pooled Plan | Experience-Rated Plan |

| How It Works | Your company’s premium risks are grouped together with thousands of other small businesses. | Your premiums are driven directly by your own team’s actual claims history from the previous year. |

| Best Suited For | Startups and expanding SMEs (Under 20 staff). | Larger, established businesses (20+ staff). |

| Rate Stability | High. Your rates are insulated against individual high-dollar claims. | Low. Your monthly costs fluctuate based on your team’s direct benefit usage. |

| Cost Driven By | The overall claims performance of the insurer’s entire small-business pool. | Your team’s specific extended health, prescription drug, and dental claims. |

| Strategic Focus | Maintaining predictable, fixed budgeting during your early growth stages. | Capturing direct cost savings once your larger headcount matures. |

To see how these models play out in reality, look at these two contrasting scenarios:

Scenario 1: An engineering firm in Edmonton grew from 8 to 22 employees over three years but remained on a Pooled Plan, paying a flat $185 per employee monthly.

The Problem: Their workforce was young and healthy, meaning their actual insurance claims were well below the pool’s average.

The Financial Hit: By staying pooled too long, they were blindly subsidizing higher-risk companies, overpaying roughly $35 per staff member every month. This resulted in over $9,200 annually in lost savings.

Scenario 2: A startup with only 10 staff opted for an Experience-Rated Plan, chasing lower upfront rates based on its historically low usage.

The Problem: During the year, a single employee required a $20,000 specialty drug.

The Financial Hit: Because the risk was concentrated on just 10 people, this single high-dollar claim destroyed their claims ratio, triggering a 30%+ renewal premium spike, a budget shock that a small startup simply cannot absorb.

Rather than focusing only on the lowest premium, SMEs should evaluate how each funding structure aligns with their workforce size, financial tolerance, and long-term growth plans.

Deploy Strategic Prescription Drug Controls

Prescription drugs represent the single largest and most volatile cost driver in Canadian group benefits. To insulate your corporate budget from a single high-cost prescription, build these three structural parameters into your drug plan:

- Mandatory generic substitution: Encourages lower-cost equivalent medications where appropriate.

- Prior authorization: Requires insurer approval before certain high-cost specialty drugs are covered.

- Annual drug maximums: Limit extreme claims exposure and improve cost predictability.

However, choosing the right funding model and claims controls is only part of maintaining a sustainable plan. Long-term employee well-being also plays an important role in overall claims performance.

Use Preventative Wellness as a Financial Shield

Many disability and extended absence claims are linked to unmanaged stress, burnout, or untreated mental health conditions.

Providing employees with early access to wellness support may help reduce absenteeism, improve productivity, and lower long-term disability risk over time.

Many SMEs implement Employee Assistance Programs (EAPs) because they offer confidential counselling and wellness resources through a predictable per-employee pricing model. Employers may also include services such as counselling, physiotherapy, virtual healthcare, or paramedical coverage with reasonable annual limits.

The goal is not to discourage employees from using their benefits, but to build a plan that supports employee wellbeing while remaining sustainable as the business grows.

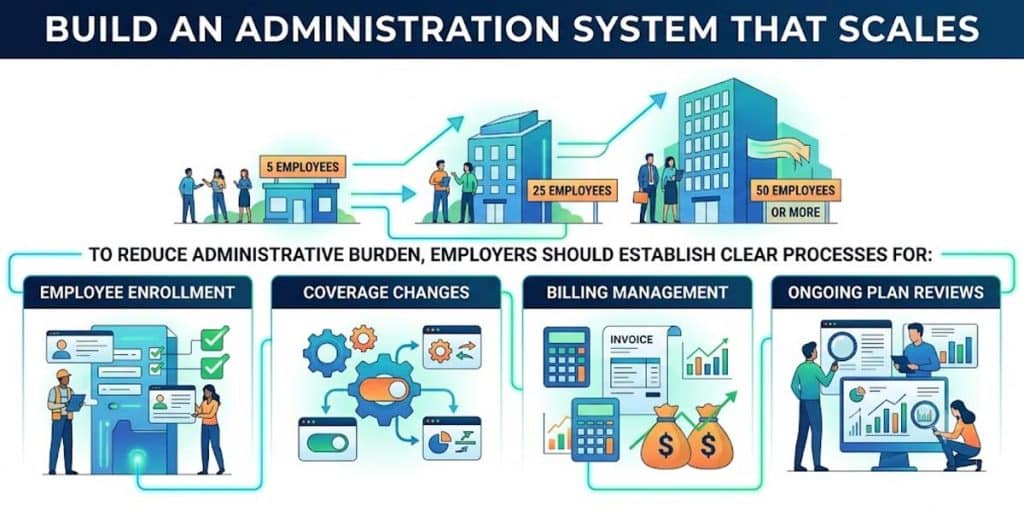

Step 4: Build an Administration System That Scales

A scalable benefits plan should be easy to manage as the workforce grows. Processes that work for a company with five employees may become time-consuming and error-prone when the organization reaches 25, 50, or more employees.

To reduce administrative burden, employers should establish clear processes for employee enrollment, coverage changes, billing management, and ongoing plan reviews.

Standardize Employee Enrollment and Eligibility Processes

As hiring picks up, it can be hard to keep track of waiting periods, enrollment forms, and employee eligibility.

Establishing a consistent enrollment process helps ensure employees receive the correct coverage at the right time while reducing the risk of missed deadlines or administrative errors. Many employers use digital enrollment tools or standardized onboarding workflows to simplify benefits administration as the workforce grows.

Create Clear Procedures for Employee Terminations and Coverage Changes

Workforce growth is often accompanied by employee turnover, promotions, leaves of absence, and other employment changes that may affect benefits eligibility.

Documented procedures for terminations and coverage updates can help employers maintain accurate records and reduce the risk of overpayments, coverage gaps, or administrative disputes.

Monitor Billing and Reconcile Benefits Costs Regularly

Benefits administration continues even after employees enroll. As the number of employees changes, employers should regularly check insurer invoices and compare them to active employee lists.

Routine billing checks can help find mistakes, ensure correct premium payments, and give better insight into overall benefits spending.

Use Renewal Reporting to Support Future Decisions

Annual renewals provide an opportunity to evaluate whether the plan continues to meet workforce needs and business objectives.

Reviewing claims trends, participation levels, cost drivers, and employee feedback can help employers identify potential improvements before making changes to coverage or plan design. This information can also support future budgeting and long-term benefits planning.

A scalable administration system helps employers spend less time managing benefits and more time making strategic decisions as the business grows.

Step 5: Communicate Benefits Clearly to Your Team

A strong group benefits plan only creates value when employees understand how to use it and recognize its importance.

As your business grows, benefits communication should focus on four areas: simple onboarding, ongoing visibility, and helping employees understand the full value of their compensation package.

Simplify Benefits Onboarding

Benefits onboarding should focus on practical information rather than lengthy policy documents. A simple summary of benefits, instructions for claims, and a short recorded guide can help new employees understand their coverage and resources.

Keep Benefits Visible Throughout the Year

Employees often forget about benefits they don’t use frequently or may not know about new resources available in the plan. Sending regular reminders can help them stay aware and make better use of these benefits. For example, employers may highlight:

- Unused Health Spending Account (HSA) balances

- Mental health and counselling services

- Virtual healthcare access

- Paramedical coverage is available through the plan

Show Employees the Full Value of Their Compensation

Many employees focus mainly on their salary and may not realize how valuable employer-funded benefits are. Compensation summaries or total rewards statements can help employees see how much the company invests in their well-being.

For example:

- Base Salary: $65,000

- Company Investment in Health and Retirement Benefits: $4,500

- Total Compensation Value: $69,500

Helping employees understand and use their benefits can increase appreciation for the plan without increasing benefits costs.

Step 6: Review Your Plan Annually and Work with a Benefits Advisor

In Canada, group benefits plans are typically reviewed and renewed once a year. Instead of seeing this as just another task, Canadian SMEs should treat it as an important opportunity. This can help them save money and provide better value for their employees.

To navigate this process successfully, your annual strategy should focus on two key actions: Review Your Plan Annually and Work Closely with Your Benefits Advisor.

Review Your Plan Annually

To avoid large and disruptive plan restructures down the road, SMEs should build a habit of regular annual evaluations. Although most insurers send renewal packages roughly 60 days before the policy renewal date, your internal review should begin a few months earlier.

Use this annual renewal checklist to assess your current plan:

- Are employees actively using the benefits that matter most?

- Are there underused benefits that could be reallocated toward higher-value coverage?

- Does the current funding structure still fit the company’s size and claims patterns?

- Have hiring plans or workforce changes created new benefits priorities?

Gathering this internal data early gives you a clear picture of what is working and what needs adjustment before you sit down with an expert.

Work Closely with Your Benefits Advisor

A good benefits advisor can help SMEs benchmark their plan against similar businesses, explain renewal increases, answer complex claims questions, and recommend ways to improve cost stability or employee value.

In Canada, group benefits brokers are typically compensated through commissions already built into the premiums charged by the insurance carrier. This means you generally do not pay any out-of-pocket fees to get a broker working on your behalf.

By combining your internal performance data with your advisor’s market expertise, you can confidently negotiate with insurers and adapt your benefits plan gradually as your business evolves.

Why Scalability Matters for Your Group Benefits Plan

A benefits plan that works for a five-person company might become hard to manage as the company grows to 20, 50, or more employees. Without a plan that can grow with them, SMEs often face higher costs, more administrative work, inconsistent employee experiences, and challenges in making changes to the plan later.

By contrast, a scalable benefits strategy allows businesses to adapt more smoothly as workforce needs, hiring plans, and operational demands evolve over time.

The difference between reactive decision-making and long-term scalable planning often becomes visible in several key areas of business operations:

| Reactive Approach | Scalable Approach |

| Adding or changing coverage only after retention issues appear | Building a flexible structure that can expand gradually as employee needs evolve |

| Responding to renewal increases without a long-term cost strategy | Planning for growth, claims trends, and contribution changes in advance |

| Managing onboarding, payroll, and benefits separately through manual processes | Using integrated systems that simplify administration as headcount increases |

| Revisiting plan structure only after major problems emerge | Reviewing and optimizing the plan regularly as the business grows |

The good news for growing businesses is that scalability does not necessarily require the most expensive plan or the most complex coverage structure from the beginning.

Strong group benefits strategies begin with a solid foundation, clear cost controls, efficient administration systems, regular yearly reviews, and consistent communication with employees.

As your company grows, these initial choices become more important. A good benefits plan can help keep employees, support their wellbeing, simplify management, and lead to more predictable long-term costs.

Scalability is not just about managing expenses. It’s about creating a benefits structure that supports both your employees and your business as it changes over time.