Form T2125 is the CRA document designed to declare business or professional income in Canada. It allows you to accurately report your earnings and claim every deduction you are entitled to.

To report correctly, you first list your total earnings as gross income. From there, subtract your allowable expenses, such as advertising, office supplies, vehicle costs, and business-use-of-home expenses. Your net income is what remains, and this final amount determines your income tax and mandatory Canada Pension Plan (CPP) contributions.

Understanding which deductions you can claim and the specific rules that govern each category ensures you only pay tax on what you actually earned and avoid common filing errors that trigger CRA reviews.

What is Form T2125?

Form T2125, Statement of Business or Professional Activities, is the CRA document used by self-employed individuals to report their business or professional income and expenses for the tax year. Form T2125 is not filed on its own but is a key part of your T1 Income Tax and Benefit Return. It streamlines your tax reporting by consolidating both business and professional activities into a single comprehensive document, replacing the older T2124 and T2032 forms.

The primary function of the T2125 is to calculate your net business income by subtracting eligible expenses, such as advertising, office supplies, and vehicle costs, from your total gross revenue. This calculation is critical because it determines the exact amount of income subject to tax and mandatory Canada Pension Plan contributions. Ultimately, the figures reported on this form will determine whether you owe a balance or are entitled to a refund.

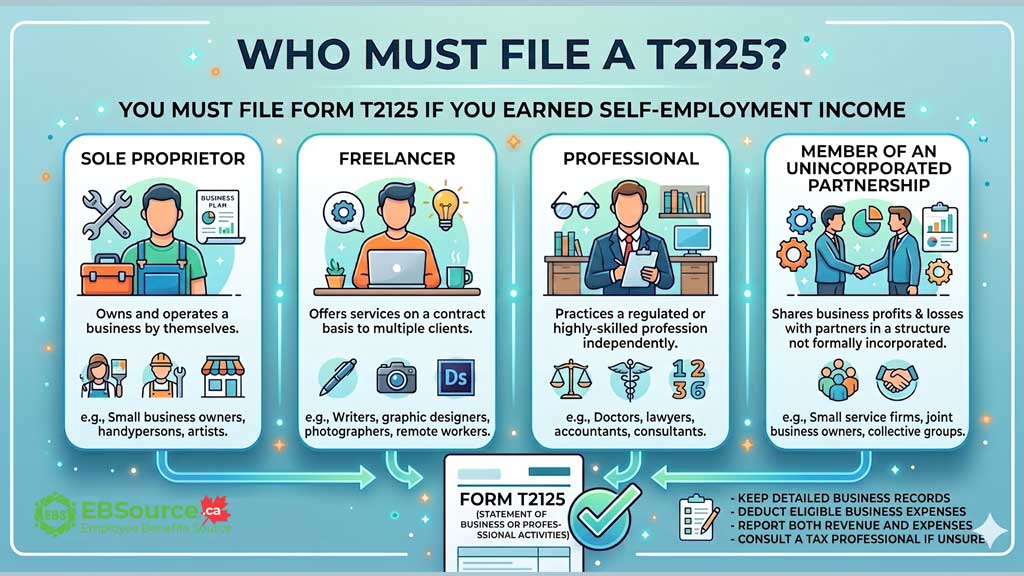

Who Needs to File a T2125 Form?

You must file Form T2125 if you earned self-employment income as a sole proprietor, freelancer, professional, or member of an unincorporated partnership.

Common examples of individuals who need to file a T2125 include:

- Sole proprietors who operate a business under their own name or a registered business name.

- Freelancers and independent contractors who provide services and receive payment without employer deductions.

- Licensed professionals such as doctors, lawyers, accountants, and engineers who earn professional fees.

- Self-employed commission earners who are not employees receive commission income from an employer.

- Partners in unincorporated partnerships with five or fewer members who each report their share of income.

Each of these filers must complete a separate copy of Form T2125 for every distinct business or professional activity they carry on during the tax year.

It is important to note that certain types of income earners do NOT use Form T2125, including Incorporated businesses, farmers, fishers, larger partnerships, and employees earning commission income. If you fall into one of these categories, the CRA requires a different form:

- Incorporated businesses file a T2 Corporation Income Tax Return

- Farmers use Form T2042

- Fishers use Form T2121

- Some partnerships must file a T5013 Partnership Information Return when they meet CRA filing criteria (for example, certain revenue/expense or asset thresholds, tiered structures, or specific partner types)

- Employees earning commission income use Form T777 for employment expenses

The CRA distinguishes between self-employment and employment based on factors such as control over work, provision of equipment, and potential for profit or loss. If you are unsure whether your income qualifies as self-employment income, read the CRA’s guidance in publication RC4110.

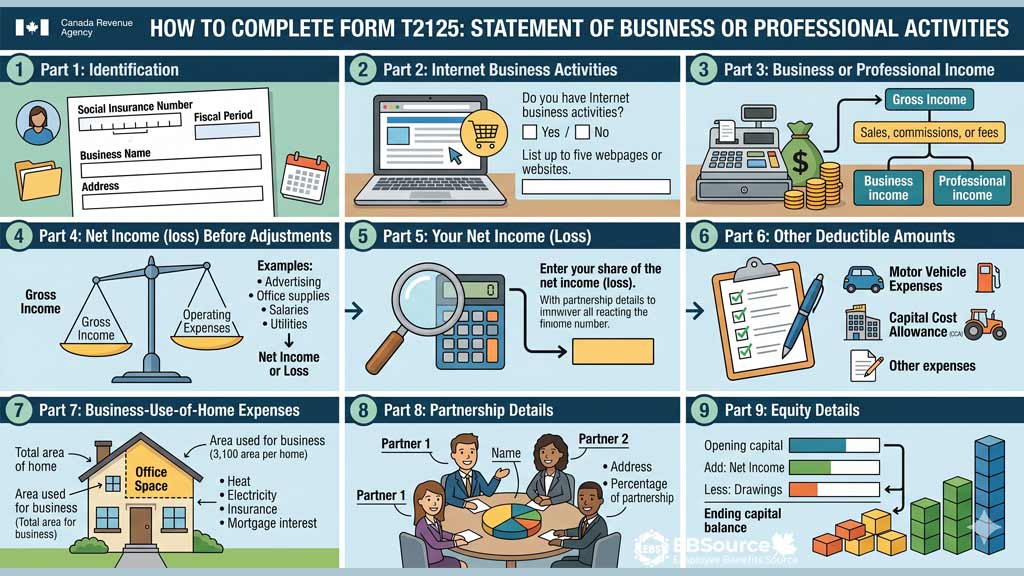

How to Complete Form T2125: A Section-by-Section Guide

Form T2125 contains nine parts, which progress logically from business identification through income reporting, expense deductions, and specialized calculation areas, with each part building on information entered in previous sections.

Completing the form correctly requires working through each section in order:

Part 1: Identification

This section collects your name, Social Insurance Number (SIN), business name, business address, type of ownership (sole proprietorship or partnership), fiscal period start and end dates, your nine-digit business number if you have one, and your six-digit industry code selected from the CRA’s North American Industry Classification System (NAICS) list. If you operate within a partnership, you also enter the partnership name and your ownership percentage.

Part 2: Internet Business Activities

This section asks whether your business earned any income through a website or online platform during the tax year. If the answer is yes, list your pages/website addresses. Then, enter the estimated percentage of your gross income generated from web pages/websites overall. If you cannot reliably calculate an exact percentage of the total, the CRA accepts a reasonable estimate.

Part 3: Business or Professional Income

This is where you report your gross revenue before any expenses. You will report either business income (Part 3A) or professional income (Part 3B). If you earn both business and professional income or operate multiple businesses, you need to file a separate Form T2125 for each distinct activity.

If you are a GST/HST registrant using the standard accounting method, report your gross sales excluding the sales tax you collected. If you are not registered or if you use the Quick Method of Accounting, the CRA has specific lines (like Line 8290) to handle the tax inclusion appropriately.

Part 4: Net Income (loss) Before Adjustments

This section presents a line-by-line list of deductible expense categories, such as advertising, meals, debt, insurance, interest, office expenses, salaries, and professional fees. To be deductible, an expense must be incurred to earn business income, and the cost must be reasonable.

Let’s break down the major expenses you can claim:

Advertising

You can deduct the full cost of advertising directed at a Canadian market through Canadian media outlets. Advertising placed in non-Canadian publications or broadcasts that target the Canadian market may be subject to deduction limits or may be disallowed entirely, depending on the medium and its Canadian content proportion.

Meals and entertainment

In most cases, you can deduct 50% of meal and entertainment expenses incurred to earn business income. For example, if you spend $80 on a business lunch with a client, the deductible amount is $40. However, there are specific exceptions. Use CRA’s Line 8523 guidance to confirm if an exception applies to your situation.

Insurance

Premiums for business-related policies are deductible, including commercial liability insurance, property insurance on business premises or equipment, and professional malpractice or errors-and-omissions coverage. Personal life insurance and personal health insurance premiums do not qualify.

Interest and bank charges

Interest on money borrowed for business purposes is deductible, along with fees your financial institution charges for maintaining a business bank account. The loan must have a direct connection to your business activity; interest on personal borrowing is not deductible.

Legal, accounting, and professional fees

Fees paid to lawyers, accountants, bookkeepers, or other professionals for services related to your business are deductible. This covers tax return preparation for the business portion of your return, legal advice on business contracts, and ongoing bookkeeping. Fees tied to acquiring a capital property are generally capitalized rather than expensed.

Office expenses

Use this line for day-to-day office operating costs that are current expenses (not capital property). Common examples include paper, pens, printer ink, postage, and small desk supplies. These must be items used up within a short period, rather than assets with a useful life extending beyond the current year.

If an item is a capital asset (for example, equipment/furniture that provides value beyond the year), it generally isn’t claimed as an “office expense”. CRA generally expects you to handle it under capital cost allowance (CCA) rules.

A Complex Area: Understanding Capital Cost Allowance for Business Assets

You cannot deduct the full cost of a major asset (like a computer, vehicle, or office furniture) in the year you buy it. Instead, you deduct a portion of its cost each year through Capital Cost Allowance (CCA). It is the tax deduction for the declining value of capital assets.

Assets are grouped into CCA classes, each with a specific rate. For example, computers (Class 50) have a 55% CCA rate, while office furniture (Class 8) has a 20% rate.

This is a complex area, and using tax software or consulting a professional is highly recommended to ensure you are claiming CCA correctly.

Salaries, wages, and benefits

Gross wages paid to your employees are deductible, along with your employer’s share of Canada Pension Plan contributions and Employment Insurance premiums. You cannot deduct amounts paid to yourself as the owner of a sole proprietorship, because your net business income already represents your compensation.

Travel

Transportation, accommodation, and meals (at 50%) incurred when you travel away from your metropolitan area for business are deductible. Eligible costs include airfare, train or bus tickets, hotel stays, and taxi or ride-share fares. Any personal portion of a trip, such as a vacation extension, must be excluded.

Telephone and utilities

The business-use portion of your telephone, mobile phone, and internet service is deductible. If a line or service is shared between personal and business use, you must calculate a reasonable business-use percentage and claim only that portion.

Supplies

Materials consumed directly in delivering your product or service qualify as supplies. For a carpenter, this might include lumber and fasteners; for a consultant, it might include printed client reports. Supplies differ from office expenses in that they relate directly to service or product delivery rather than general administration.

Motor vehicle expenses (not including CCA)

If you use your personal vehicle for business, you can deduct a portion of its operating costs, such as fuel, insurance, registration, maintenance, and loan interest or lease payments.

The CRA requires detailed records to support your claim. You must track your total kilometres driven for the year and the kilometres driven specifically for business errands (e.g., visiting clients, picking up supplies).

Other expenses

Any legitimate business expense that does not fit into a named category can be claimed here, provided it meets the general deductibility conditions. Clearly describe the nature of each expense so the CRA can assess its validity if the return is reviewed.

Part 5: Your Net Income (Loss)

Subtract total expenses from gross profit to calculate net income. If the result is positive, it adds to your taxable income. If it’s a loss, you may be able to use it to reduce other income, but only if your business shows a real intent to make a profit. For partnerships, adjust for your share of the partnership.

Part 6: Other Deductible Amounts

This section is for expenses that don’t fit into other categories. For example, management fees paid to related parties or international transaction fees for foreign sales qualify. Be careful not to claim the same expense in more than one section.

Part 7: Business-Use-of-Home Expenses

CRA rules generally allow you to claim the business portion of eligible home expenses if your home is your principal place of business, or if it is used only to earn business income and used to meet clients/customers/patients on a regular basis

Your claim is limited by your business income for the year. Calculate the square footage of your workspace divided by the total square footage of your home; then, apply this percentage to your rent, utilities, property taxes, home insurance, etc. Note that commission earners and standard business owners have slightly different eligible expenses.

A Note on Loss Restriction: You cannot use home office expenses to create or increase a business loss. For example, if your business net income is $2,000, and your home office expenses are $3,000, you can only deduct $2,000. The remaining $1,000 carries forward to the next tax year.

Part 8: Partnership Details

These sections capture the allocation of net income among partners if you are in a partnership. List each partner’s name, SIN, and share of profit or loss. Make sure these details match your partnership agreement.

All partners must use the same fiscal year and reporting methods. If not, CRA may audit the entire partnership.

Part 9: Equity Details

This section summarizes items such as business liabilities, drawings (owner withdrawals), and capital contributions (owner funds put into the business).

If you pay business costs using a personal card/account, track it consistently in your records (for example, as an owner contribution and a business expense), so your totals for drawings/contributions remain supportable.

Choosing a Filing Method for Your T2125

The T2125 accompanies your T1 personal tax return through three filing methods: NETFILE using certified tax software, EFILE through tax professionals, or paper filing mailed to your provincial tax centre.

Each method has its own advantages in terms of speed, cost, and professional oversight:

NETFILE (online filing)

Using CRA-certified tax software is the fastest way to submit your T2125 and T1 return. This method allows immediate data transmission and much faster processing times than traditional mail. For the most current estimates (including electronic filing), use CRA’s Check processing times tool.

EFILE (through tax professional)

If your business activities are complex, it is advisable to hire an accountant or tax preparer to submit your return via EFILE. They know how to handle complex situations and can offer helpful advice on various business activities. This costs more than self-filing but provides expert review.

Paper Filing (mail)

While slower and less common, paper filing remains an option. You can download and print the T2125 from the CRA website, complete it manually or as a PDF, print your completed T1 return, and attach the T2125. Once finished, mail both documents to your regional tax centre.

Keep in mind that mailing addresses vary by province, so you must verify the correct destination on the official CRA website.

Important Deadlines: When to File Your Return

For 2026, CRA’s filing due date is April 30 for most people. If you (or your spouse/partner) are self-employed, your filing due date is June 15, 2026, but any balance owing is due April 30, 2026. Always confirm dates for your tax year on CRA’s due-date page.

The late-filing penalty is 5% of your balance owing plus 1% per full month late (up to 12 months). A repeated late-filing penalty can apply in some cases: 10% + 2% per full month late (up to 20 months) when CRA conditions are met (including a prior penalty and a demand to file)

Source: Interest and penalties on late taxes – Canada.ca

Four Common Mistakes to Avoid When Filing T2125 Form

Completing T2125 is tricky. Common mistakes include claiming personal expenses, keeping insufficient records, omitting income, and confusing filing and payment deadlines. Avoiding these four mistakes is the best way to prevent problems before they start:

Mixing Business with Personal Expenses

As a general rule, if an expense has both a personal and a business component, you must calculate the business-use portion and deduct only that amount. Claiming personal expenses as business deductions is one of the most common triggers for CRA reassessments.

Inadequate Record

During an audit, your claims are just claims until you back them up with proof. Essential records to keep include sales invoices and contracts documenting income, purchase receipts with vendor details and GST numbers, bank statements showing payment flows, Vehicle logbooks detailing business usage, home office calculations and supporting bills, and asset purchase documents for CCA claims.

A deduction without a receipt is just a donation to the government you didn’t have to make. Thus, keeping organized records is the best way to avoid being denied your expenses or facing expensive penalties.

Omitting Income

All income, including cash payments and barter transactions, must be reported. The CRA uses data from third-party payment processors to verify income.

Confusing Filing and Payment Deadlines

For the self-employed, there is not just one tax deadline to remember. While you have until June 15th to file your paperwork, any taxes you owe are due by April 30th. Filing on time but paying late will result in interest charges on your outstanding balance.

FAQs about T2125 Form

Is T2125 the same as T4?

No. A T4 slip is issued by an employer for employment income. A T2125 is a form you complete yourself to report self-employment income.

What’s the difference between business income and professional income?

Business income comes from selling products or general services. This includes people such as a web designer, retail shop owner, or consultant who earns business income. Most self-employed Canadians fall into this category. On the other hand, professional income applies to professions such as law, medicine, engineering, and accounting. You must hold an active membership in a provincial or territorial professional association or regulatory body.

Do I need a business number for T2125?

No, a business number is only required if you are registered for GST/HST or have employees. You can leave this field blank if you are a sole proprietor with no registrations.

Why would the CRA audit my T2125?

Audits can be random, but common triggers include reporting large business losses for several years in a row, unusually high expense claims (especially for meals, travel, or vehicle use), or inconsistencies between your T2125 and GST/HST filings.

What happens if I don't file T2125?

Failing to report self-employment income can lead to significant penalties for late filing and failure to report income, plus interest on the unpaid taxes. The CRA can reassess your taxes for several years back if unreported income is discovered.